You cannot time the housing market.

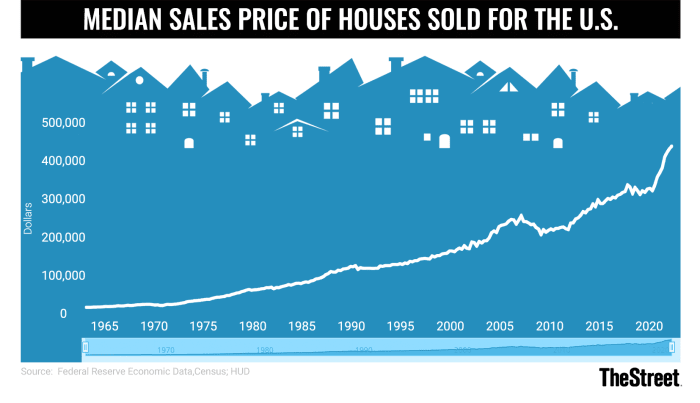

That assertion, on the floor, looks like it is mistaken, however over 50 years of gross sales information recommend broadly that the best time to purchase a home is all the time now. Housing costs, in fact, range by market, however on a nationwide degree, they’ve climbed steadily for the reason that Nineteen Sixties, in accordance with information from the St. Louis department of the Federal Reserve.

Mortgage charges, which have mainly doubled from 2.9% a 12 months in the past to five.89% as of Sept. 8, are an element, however ready for charges to drop is a harmful recreation. If mortgage charges do fall, extra persons are prone to find yourself again within the housing market. That will push costs increased.

Housing is usually, not an non-obligatory buy. Unless you might have somebody keen to offer you a spot to stay freed from cost, your selection is renting or shopping for a house, and as housing costs climb rental charges typically transfer in the identical route.

“Median rent in the top 50 metropolitan markets hit a record $1,849 in May, up 15.5% from a year earlier, according to Realtor.com, a real estate services firm. It was the 15th straight month of record rent,” TheStreet’s Dan Weil wrote in July.

Put merely, in the event you want a spot to stay, and anticipate to remain put for not less than just a few years, shopping for makes extra sense than renting.

TheStreet

Housing Prices Go Up

As you possibly can see on the chart above, housing costs transfer steadily increased. Yes, there are durations the place they dip and particular person markets might range however the best time to purchase a home has traditionally typically all the time been “now.”

Mortgage charges are an element, however they’re additionally relative. The present fee hike has slowed, if not stopped, rising costs in lots of markets. If we see decrease charges, even just a few years from now, that might be a catalyst for costs to rise once more.

Scroll to Continue

It’s essential to grasp the affect of mortgage rates of interest in your potential cost. If you borrow $300,000, here is what you’ll pay per 30 days at a wide range of rates of interest

- 3%: $1,265

- 4%: $1,432

- 5%: $1,610

- 6%: $1,700

- 7%: $1,996

That’s a $435 per 30 days distinction between the place charges had been a 12 months in the past and the place they’re now (kind of). The added value definitely elements into how a lot you possibly can spend on a home, however it typically doesn’t imply you shouldn’t purchase a home.

A Personal Look at Buying a House

During the pandemic, my spouse and I bought our downtown apartment, used the proceeds to purchase a resort apartment/rental property, and moved right into a rental. When we moved to the rental — a transfer compelled by needing to remain on my son’s bus route for his final year-and-a-half of highschool — we had been paying $2,495 a month for a 2,600 s.f. 4-bedroom townhouse in a group with a pleasant pool and a gymnasium.

That quantity was round what our prices had been within the apartment we owned beforehand, however we weren’t constructing fairness or gaining any appreciation. In 12 months two, our hire went as much as $2,700 a month and that is after we started searching for a house.

Ultimately, we determined we couldn’t afford what we needed (a 3-bedroom, single-family house) within the South Florida space the place we lived, so we started trying about 40 minutes north. Ultimately, we discovered a house in a pleasant group with comparable facilities to what we had been leaving and acquired a 3-bedroom, 1,600 s.f. single-family house for $315,000, placing 20% down.

And whereas we downsized a bit, we had by no means wanted as a lot house as we had within the rental, so having a yard, a storage, and a pleasant screened-in lanai appeared like a good trade-off. We obtained in earlier than rates of interest spiked our mortgage is at roughly 4% making our month-to-month funds, which incorporates about $400 in owners affiliation charges in addition to our insurance coverage and tax escrows about $2,1,00 a month.

That’s $600 a month lower than we had been paying to not personal a house (and $1,900 a month lower than what our earlier landlord obtained from the following tenants). If we had waited just a few months and paid 6% curiosity our cost would have gone up $330 per 30 days (and our value to purchase would have been increased as costs hold climbing).

So, now, as an alternative of renting the place prices would virtually definitely rise on a year-to-year foundation we’re constructing fairness in a property in a group the place costs are prone to climb. We, in fact, face added prices like repairs and enhancements (we redid the complete home), however we personal our house and that offers us an asset that ought to construct our wealth over time.

Source: www.thestreet.com”