A sustained excessive variety of new enterprise functions from mid-2020 to now signifies an optimism not essentially shared throughout the financial system. That ambition could also be examined within the coming months.

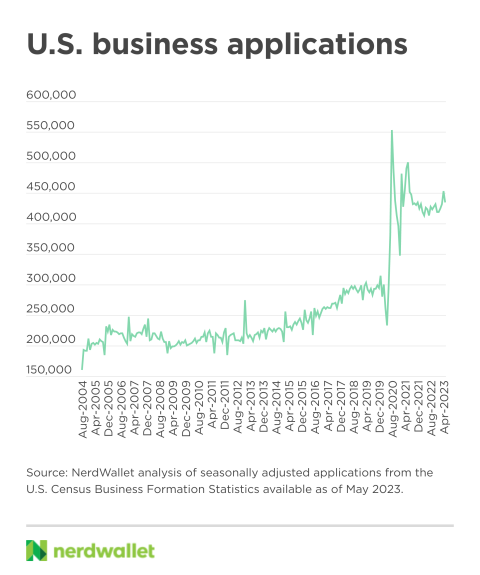

From January to July 2020 — the six-month interval with a really brief and deep recession smack dab in its center — the variety of functions for employer identification numbers (EINs) from the IRS practically doubled. That bold optimism amid nice financial uncertainty persists: As of April 2023, filings of those new enterprise functions have been 55% increased than in that January three years earlier.

But banks are being extra cautious about lending, and shoppers might start pulling again on spending after an extended marketing campaign by the Federal Reserve to chill the financial system. New companies, by their nature usually on already-vulnerable monetary footing, ought to put together for rocky occasions with the data that every one wholesome companies, younger or outdated, can profit from contingency planning.

New companies nonetheless elevated, three years after peak

COVID-19 lockdowns and layoffs inspired individuals to get inventive about how they spent their time and the way they earned and spent their cash. For many, that interval was the proverbial kick within the butt wanted to lastly chase a dream of being self-employed. The variety of new enterprise functions peaked in July 2020 at about 552,000, up from 279,000 simply six months earlier. And whereas the surge has subsided barely, it stays increased than any pre-COVID interval tracked.

Could this be proof that the pandemic did have a long-term affect on how we take into consideration work? Perhaps. It may additionally point out extra individuals are beginning aspect companies to assist them cowl the elevated prices of dwelling beneath excessive inflation, or they’re desirous to seize the elevated demand for providers that has ballooned because the pandemic has waned. Most possible, it’s a mix of things whose affect will turn out to be clearer as time goes on.

Even the companies deemed most certainly to succeed (referred to as “high propensity” by the U.S. Census Bureau) stay elevated. What identifies these companies as excessive propensity, in keeping with the company, can embrace deliberate wages and hiring, company backing, or being in sure industries corresponding to meals providers and lodging, development and manufacturing, instructional providers, well being care and others. These functions additionally peaked in July 2020, at about 175,000, 73% increased than six months earlier than. In April of this yr, there have been nonetheless 44% extra such functions than in January 2020.

All states have skilled comparable development, albeit to various levels. The states that noticed the largest will increase from January 2020 to their peak have been Illinois and Mississippi, rising 248% and 247% respectively to their July 2020 highs. In Wyoming, software charges peaked later, in April 2023, the newest month for which information is on the market. And there, they continue to be essentially the most elevated, 181% greater than the January 2020 charge.

But lenders say they’re pulling again

In the early phases of a brand new enterprise, startup and growth funding could be essential. But for brand spanking new companies in 2023, entry to those funds may show more and more troublesome.

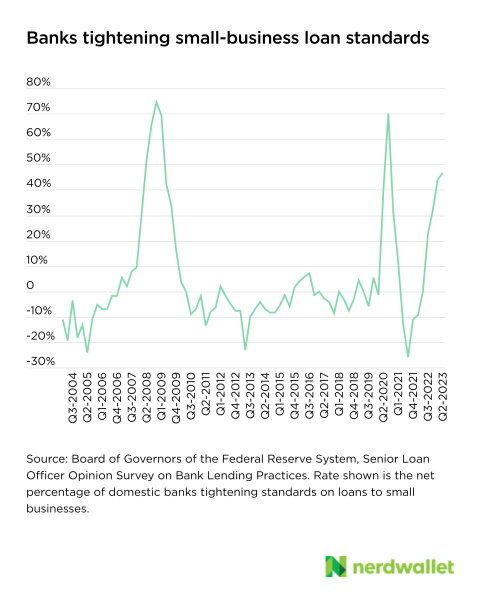

The share of home banks tightening lending requirements for small companies stood at 47% within the second quarter of this yr, up from zero one yr prior, in keeping with the Senior Loan Officer Opinion Survey from the Fed. Loan officers report comparable tightening for bigger companies, too. Lenders are most certainly to quote financial uncertainty — not banking instability — for the tightening and anticipate the pattern to proceed.

What to anticipate (and the right way to put together) for the remainder of 2023

Throughout 2023, it should stay tougher (and dear) for homeowners of all sizes of companies to entry funding. The financial uncertainty driving credit score tightening is carefully associated to the dearth of certainty round whether or not the Fed will proceed to lift charges, pause or start decreasing them; whether or not the labor market will lastly weaken; whether or not we’ll enter a recession this yr; and whether or not any extra unexpected financial shocks — like conflict or a pandemic — head our means. So companies outdated and new could be clever to hope for the most effective however plan for powerful occasions.

Prepare for falling client demand. The Fed’s battle towards inflation is an effort to chill the financial system and, partly, client demand. People might be spending much less, whether or not or not we in the end find yourself in recessionary territory. Businesses that generate profits from discretionary client spending may really feel this essentially the most.

Look for tactics to scale back bills. Think forward — you might not want to alter suppliers or cut back delivery frequency at present, however the place will you reduce if the necessity arises? Knowing the place to chop when occasions get lean permits you to take fast motion when these occasions happen.

Consider a line of credit score. A enterprise line of credit score can act as an emergency aid valve — it’s shut at hand in case you want it and usually comes with comparatively minimal carrying prices in case you don’t find yourself utilizing it. If your enterprise has unpredictable or risky money flows, it may be an at-the-ready emergency fund.

If it’s important to borrow, contemplate an area financial institution or CDFI. Now is just not a good time to want a mortgage: Rates are excessive, and lenders are watching their cash rigorously. But in case you do must borrow, contemplate an area financial institution, credit score union or group growth monetary establishment (CDFI). If you have already got a relationship with one in all these smaller establishments, you’re one step forward. Because they’re within the relationship enterprise, they might have aggressive benefits over bigger banks for smaller companies.

Ask for assist — earlier than you want it. Having a plan in place simply in case issues get dicey can present peace of thoughts even when they don’t. As a brand new enterprise proprietor, you might not know what you don’t know, and it may pay to have somebody with expertise assist inform your choices. Small Business Development Centers provide free consulting and free or low-cost coaching to small-business homeowners. And SCORE, a nonprofit that companions with the Small Business Administration, supplies mentors and sources to assist small companies succeed.

More From NerdWallet

Elizabeth Renter writes for NerdWallet. Email: [email protected]. Twitter: @elizabethrenter.

Source: www.bostonherald.com”