The Mega Initial Public Offer (IPO) of Life Insurance Corporation of India (LIC) is expected to come soon. The most important thing about LIC’s IPO is that the company can reserve a part in the IPO for its more than 25 crore policyholders and can also give them some discount. LIC is also regularly advertising how its policyholders can get their demat account opened for investing in IPOs.

Policyholders must be already aware of LIC’s insurance products. However, as a potential investor, it is also important for them to know the technical terms and their definitions that are associated with life insurance companies and their valuations.

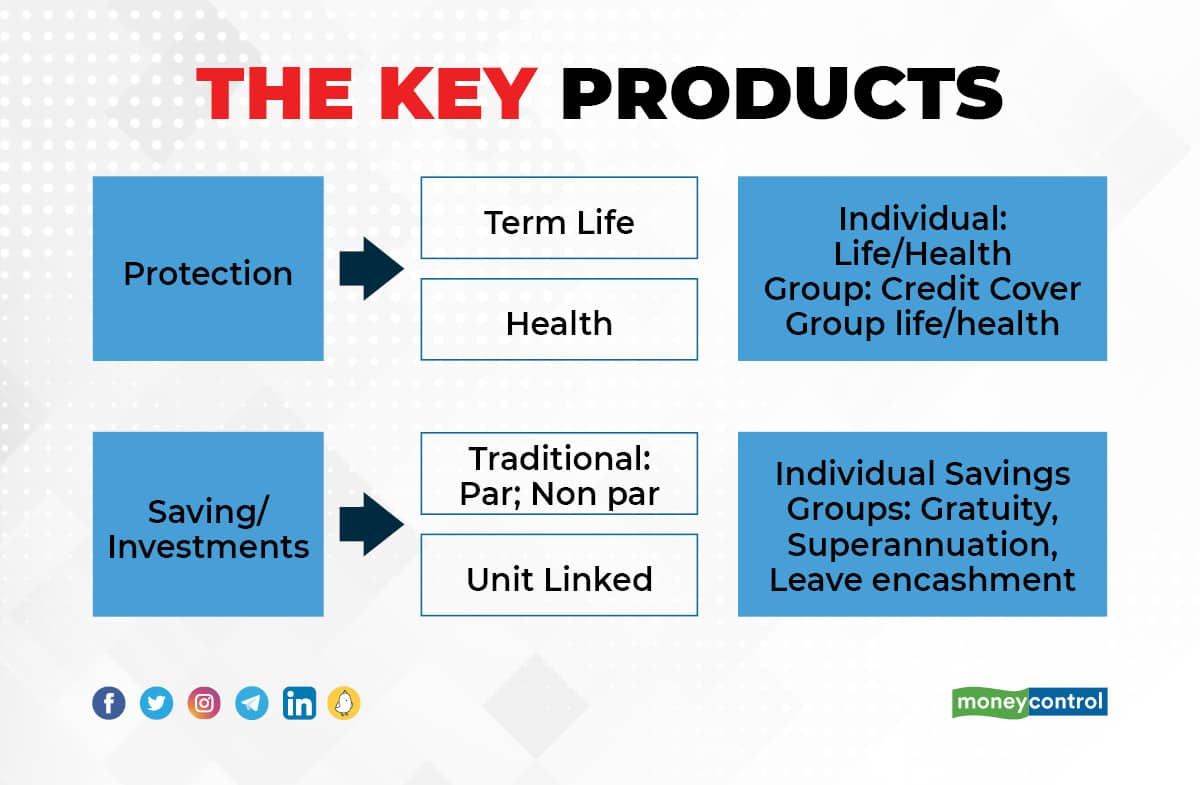

key product

Life insurance companies provide insurance cover against the risk of death and critical illness. In addition, she also offers some savings products. The company’s products include schemes like Term Insurance, Pension Plans, Unit-Linked Savings Plans (ULIPs), Annuities, which are tailored keeping in mind the needs of the policyholder.

protection business

Individual term life products cover only the risk of death and pay out only in the event of death. If the policyholder survives for the entire term, nothing is paid to him. Whereas group products involve dealings at the business level and include products such as group credit, group life and group health.

savings business

The main objective of a savings plan is to earn a return on investment with a long-term investment horizon. It has a life cover plus a maturity amount, which is generally less than a term insurance plan. Savings products can be divided into two categories – traditional products (participating products and non-participating products) and unit-linked products (ULIPs).

Participating: In this, a minimum return is guaranteed and policyholders take the benefits of the policy into consideration. Under the rules in India, the surplus profit is divided in the ratio of 90:10. Of this, 90 percent is given to the policyholders and 10 percent to the shareholders.

Non-participating: In this, full payment is guaranteed at the very inception of the policy. Policyholders do not share in the benefits of the policy.

ULIP: These offer market linked returns and the amount the policyholders will get depends on the fund’s performance in the market.

group saving product: These are fund management products, where insurance companies manage funds for large business groups. For example: Gratuity, Retirement and Leave encashment.

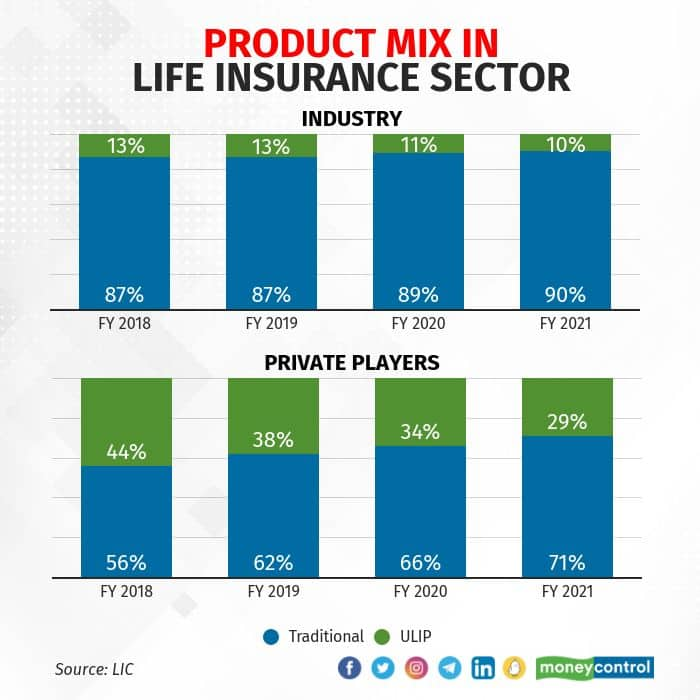

product mix

Product mix is an important aspect which should be taken care of. The product mix itself supports the margin and profits of the insurance company. Many private insurers want to increase the share of protection business (pure term life insurance) in their product mix as it gives them higher margins as compared to ULIPs.

You can understand the status of the product mix in the insurance sector with the help of this graph-

solvency ratio

Solvency ratio is the amount of capital required to run an insurance company. It is decided keeping in mind the portfolio of policies of the insurance company. Under the existing rules, the minimum solvency ratio at all times should be 150%.

embedded value

Embedded value plays a very important role in the valuation of any insurance company. It is calculated by taking the present value of all future profits of the company and adding it to the Net Asset Value (NAV). After determining the embedded value, the valuation of the company is decided on the basis of this and then on the basis of that valuation, the value of the IPO is decided.

.