Here’s a sentence which could sound just a little odd: increased rates of interest have been excellent news for the UK financial system.

For the primary time in lots of many years, the ache confronted by debtors from increased rates of interest has been greater than balanced out by the profit skilled by savers from these rates of interest.

If this sounds just a little odd it is partly as a result of invariably, when individuals – the media, politicians and economists – speak about rates of interest they focus unduly on one facet of the equation: the plight of the borrower. And there’s an comprehensible motive for that: in earlier “hiking cycles”, when the Bank of England raises rates of interest, that ache has invariably outweighed the windfall.

Money newest: Mortgage value warfare ‘possible’ as 3% rates of interest predicted

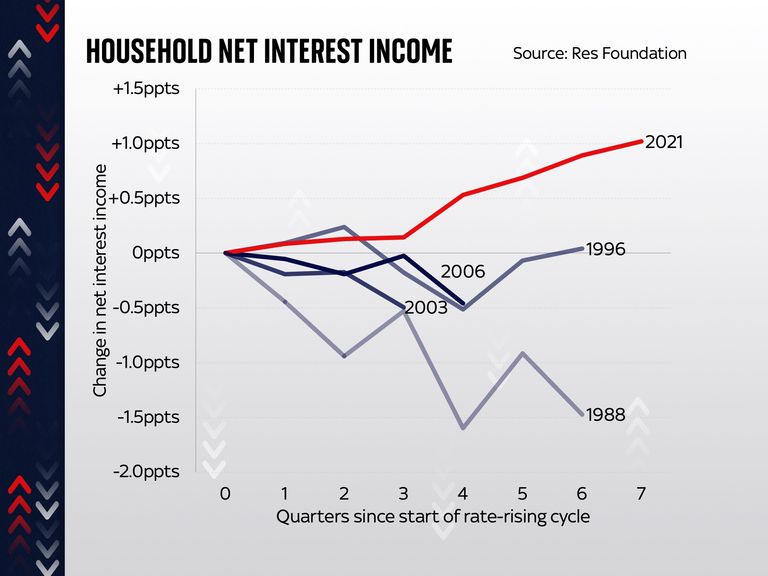

That was the case when borrowing charges had been lifted in 1988; it was the case in 1996, in 2003 and in 2006.

In every case the general affect, throughout the financial system, on households’ stability sheets was unfavorable.

But not so this time round.

According to the Resolution Foundation, the online earnings we have earned, throughout the financial system, on account of rates of interest, has really risen moderately than fallen – up by a proportion level since charges began going up.

To put that into perspective, the “interest rate effect” on incomes within the late Eighties was -1.5 proportion factors.

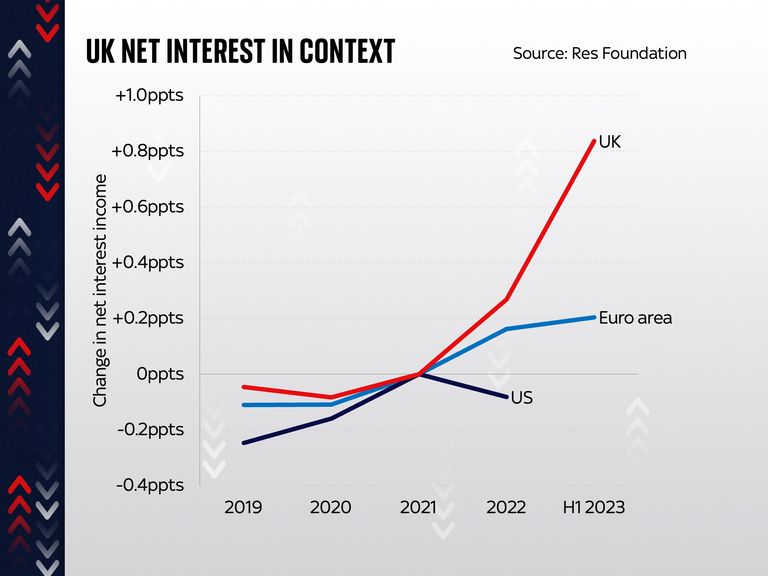

And what’s placing, once you examine the UK to the euro space and the US, is that we’re a little bit of an outlier: the rate of interest impact, throughout the financial system, was way more constructive than it was in these two different areas.

This, says the Resolution Foundation, is not less than a part of the reason for a way the UK hasn’t but slipped into the recession lots of people anticipated this time final 12 months.

Part of the reason for that is that it so occurred, largely due to the pandemic lockdowns, that individuals started this mountaineering cycle with a whole lot of financial savings of their financial institution accounts – excess of ordinary.

Read extra:

Mortgage approvals up as extra lenders minimize charges

First-time patrons fall to ‘lowest stage in a decade’

FTSE 100 bosses ‘earn typical UK annual wage in three days’

The upshot was that, throughout the financial system, the profit from these financial savings (and financial savings charges went up in a short time – albeit to not the degrees of borrowing charges) was better than the affect on mortgages and loans. Another a part of the reason is that thus far solely round half of these with fixed-rate mortgages have re-fixed their loans.

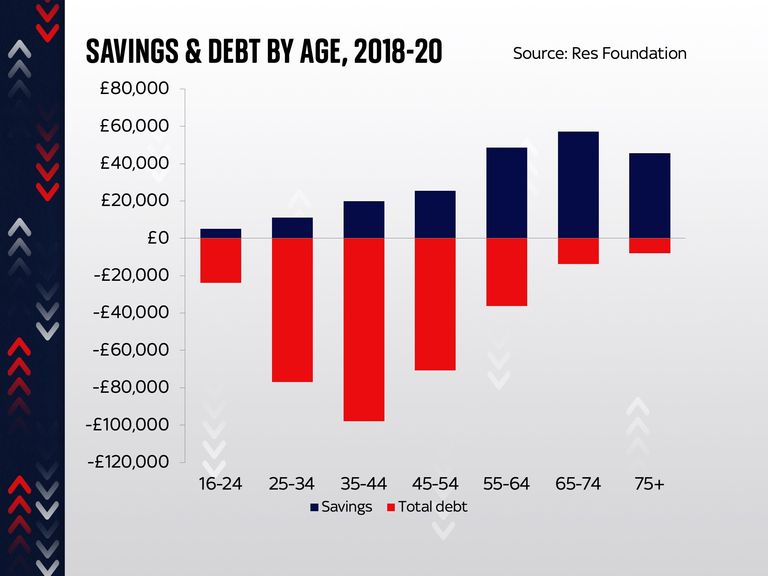

But there are just a few crucial provisos right here. The first and maybe most vital is that whereas the above is definitely true throughout the entire financial system, there is a dramatic distinction of expertise for various classes of individuals.

Those whose money owed outweigh their financial savings (which on this case principally means youthful individuals) will definitely see a unfavorable affect from increased charges. Those with much more financial savings than money owed – the older segments of the inhabitants – will see a profit. In different phrases, the ache and the dividends will not be being equally shared out. The previous are doing a lot better; the younger are doing worse.

And there are two different provisos. The first is that this constructive affect will start to put on off as increasingly individuals re-fix their mortgages and go up from low-interest charges to increased charges. Even although the standard fixed-rate deal has been coming down lately, it is nonetheless far increased than it was two or 5 years in the past.

Click to subscribe to The Ian King Business Podcast wherever you get your podcasts

The remaining proviso is that not one of the above takes into consideration the broader affect of the price of dwelling disaster.

Everyone is having to pay increased costs for practically every thing. And whereas the annual price at which these costs are growing (inflation) has decelerated, the extent of costs stays greater than 15% above the place it was a few years in the past.

That’s a painful adjustment for everybody. The excellent news is that the affect of charges – throughout the financial system as an entire – has really been constructive moderately than unfavorable. But not everybody will likely be seeing the advantages.

Source: information.sky.com”