The Takeaway: The median internet value of married {couples} within the U.S. is larger than the online value of single individuals in any respect age ranges.

The comic Henny Youngman as soon as stated that the key to a contented marriage stays a secret.

But the king of 1 liners was fortunately married for 59 years. So he and his partner Sadie had been clearly in on the key.

DON’T MISS: U.S. Net Worth: What Makes Up Household Wealth?

Here’s one thing that’s not a secret, only a truth: married {couples} are likely to have a larger internet value than their single counterparts.

The monetary advantages of marriage have lengthy been identified, however they could be even larger than you assume.

A latest report from the U.S. Census Bureau discovered a big correlation between an individual’s marital standing and their family wealth, primarily based on an examination of the 2022 Survey of Income and Program Participation (SIPP).

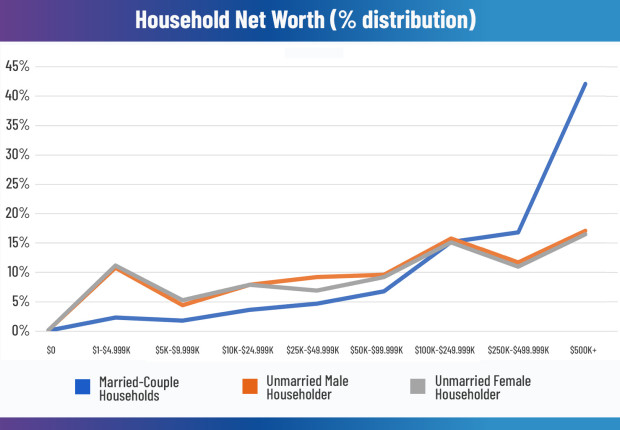

The median internet value of married-couple households, the researchers discovered, was larger in any respect age ranges than that of households headed by single individuals.

U&interval;S&interval; Census Bureau, 2022 Survey of Income and Program Participation, public-use information

Married homeowners underneath the age of 35 had a internet value 9.2 occasions greater than single feminine homeowners and three.1 occasions greater than single male homeowners. Between the ages 35 and 54 — a time of life when many individuals purchase their largest asset: a house — the median wealth of married {couples} surpassed that of single individuals at an excellent larger clip.

“This pattern suggests that the gaps in median wealth cannot solely be attributed to the presence of an additional adult in the household,” the report stated. “Otherwise, married households would have no more than twice the median wealth of unmarried households.”

Compare the Best Savings Rates

The Census outlined internet value, or wealth, as the worth of property owned minus the money owed owed. It included property resembling house fairness, automobiles, investments, and financial institution accounts. The main property not included had been fairness in pension plans and the worth of house furnishings.

Millennials and Marriage

So what’s inflicting this specific wealth hole, and will it get larger?

A 2019 research by the Federal Reserve Bank of St. Louis factors to some explanations. As fewer younger adults tie the knot within the twenty first century, the Fed reported, marriage has develop into more and more stratified.

“Shifting trends in family structure over three decades combined with an increasing concentration of assets contributed to a smaller share of young adult households, i.e. married couples, having a larger concentration of housing wealth,” the report stated. In different phrases, marriage typically results in homeownership.

U&interval;S&interval; Census Bureau, 2022 Survey of Income and Program Participation, public-use information

At the identical time, the Fed famous, “a growing proportion [of young adults] — unmarried young adults — have more financial vulnerability, specifically debt, during this transitional phase of the life course.”

The Fed additionally highlighted analysis indicating that progress in scholar debt ranges is related to delaying or avoiding marriage, suggesting “that young adults increasingly feel that their debt is an economic barrier to transitioning to adulthood and forming a family.”

Young households had been significantly affected by the Great Recession of 2008, the Fed report famous, however single younger adults had stability sheets that “continue to look particularly vulnerable 10 years after the economic downturn.”

Gender and Net Worth

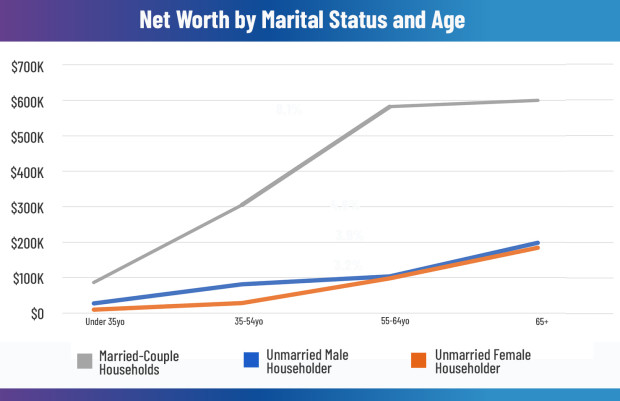

According to the Census report, family wealth was increased with age, no matter marital standing. But married {couples} continued to say the very best internet value of all age teams — and single girls the bottom. (The report did not specify if same-sex married {couples} had been included within the married homeowners group.)

Married {couples} aged 65 and older had a median internet value of $600,000. The median internet value for single male homeowners and single feminine homeowners of the identical age was $197,900 and $184,000, respectively.

“Large gender wealth gaps indicate that many women-headed families have smaller financial cushions than those families headed by men,” The Fed wrote in 2021. “Savings and other assets blunt the impact of personal economic crises like losing incomes or being laid off, which occurred disproportionately for women during the COVID-19 recession.”

Half of households had been headed by girls, but they owned solely 28% of complete family wealth as of 2019, the Fed famous. When mixed with race, the gender wealth hole was even wider, with Black and Hispanic girls proudly owning simply pennies on the greenback in contrast with white males.

Source: www.thestreet.com”