It’s early Sunday morning, and the silence of an extended week is damaged by the sound of Mr. Smith’s cellphone on his nightstand. It’s the hospital calling about his daughter, who has been injured and is in intensive care.

Mr. Smith rattles off query after query about how his daughter is doing with solely imprecise generalities in response. The attending physician asks whether or not Mr. Smith occurs to have a HIPAA authorization or well being care surrogate for his daughter. Mr. Smith ignores the query and repeats his considerations about his daughter’s accidents. The physician continues to skirt across the problem and return to what appears to be an pointless dialogue about authorized paperwork. How might this be?

Legal Matters

A whole lot of modifications when your youngster turns 18 and heads off to school. Going out on their very own is a big stepping stone in attaining individuality, however what most mother and father and college students don’t understand is that there are large authorized modifications that happen when your youngster turns into an grownup.

When your youngster turns 18, you may not make authorized choices for them or retrieve details about them that’s thought of non-public with out their written permission. And sadly, there isn’t only one single authorized doc to deal with this drawback. In reality, there are 4 vital paperwork that each grownup ought to put together. These key authorized devices can assist to make sure that any sudden circumstances your loved ones faces generally is a little much less burdensome.

BIO| Jamie Hargrove, CPA, Attorney

Bio: Jamie Hargrove, CPA, Attorney

Healthcare Power of Attorney

Also often known as a healthcare proxy, this doc offers mother and father the power to make choices about their youngster’s healthcare. If a scholar goes to high school out of state, it’s prudent to have a healthcare energy of lawyer from each states, since some healthcare professionals could also be hesitant to just accept an authorization kind they don’t acknowledge.

HIPAA Authorization

This doc permits healthcare professionals to share a scholar’s in any other case confidential healthcare info with the individual or individuals the scholar needs.

Living Will Declaration

Sometimes known as an superior care directive, the dwelling will declaration is a vital doc that, in response to a 2020 Gallup ballot, fewer than half of the U.S. grownup inhabitants possesses. This important doc does the next:

- Tells physicians and medical groups, in addition to members of the family, how a affected person desires medical care dealt with in a vital state of affairs. It specifies the affected person’s values and what’s necessary in therapy, particularly when circumstances are life-threatening.

- Protects sufferers from undesirable and, in some instances, an pointless medical intervention which can solely delay demise and can lead to continued ache and struggling.

Financial Power of Attorney

When mother and father want to assist handle their youngster’s funds, this doc can authorize them to take action. It permits mother and father to behave on a toddler’s behalf in all monetary issues. A monetary energy of lawyer may be helpful in lots of conditions. For occasion, if a scholar has an accident or falls unwell, leaving her or him both quickly or completely unable to make monetary choices, a designee can step in to handle financial institution accounts, file tax returns, make mortgage funds, and so forth.

As talked about earlier, so much modifications when your youngster turns 18 and heads off to school. Even in case your youngster has little or no property, there are healthcare and monetary choices that have to be made and documented. So pack your scholar’s luggage, load up the automobile, fly the varsity banner, and name your lawyer.

Taxes, taxes, taxes

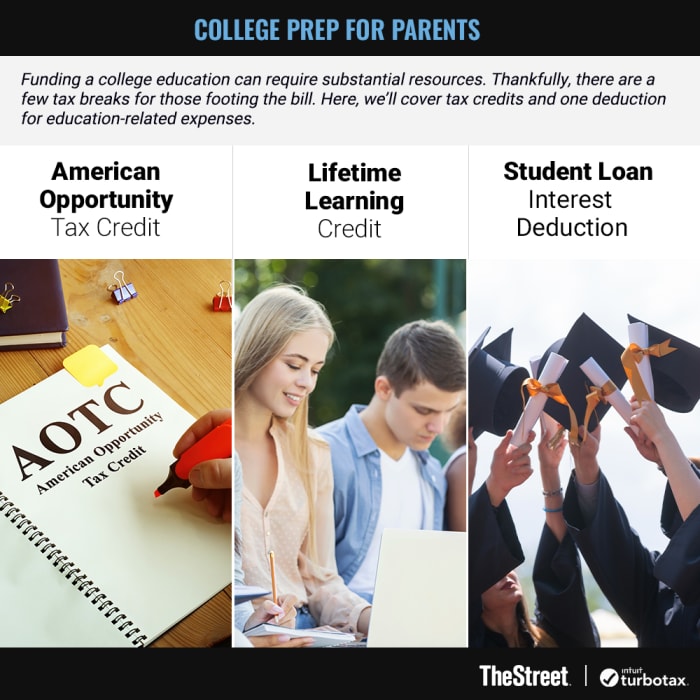

Funding a school training can require substantial sources. Thankfully, there are a couple of tax breaks for these footing the invoice. Here, we’ll cowl tax credit and one deduction for education-related bills.

Scroll to Continue

Graphic: College Prep for Parents

American Opportunity Tax Credit (AOTC)

A tax credit score of as much as $2,500 is out there per eligible scholar per 12 months starting within the tax 12 months 2021 for certified training (QE) bills. The credit score is for 100% of the primary $2,000 in QE bills and 25% of the following $2,000 in QE bills. You can qualify for the credit score in case your 2022 modified adjusted gross earnings (MAGI) is $90,000 or much less ($180,000 or much less for married submitting collectively). (For most individuals, MAGI is solely their adjusted gross earnings.)

Also, in contrast to the LLC mentioned beneath, a portion ($2,000 of the $2,500) of the AOTC is a refundable credit score. That means should you don’t owe any taxes, you may stand up to $2,000 of the AOTC refunded to you. Yep, meaning Uncle Sam sending you a verify. Nice!

It is necessary to notice that there’s a four-year most limitation per eligible scholar (together with any years of the previous Hope credit score claimed).

Lifetime Learning Credit (LLC)

While the AOTC is focused towards undergraduate training, the LLC is directed towards each undergraduate and graduate training and for programs to accumulate or enhance job expertise that aren’t part of the AOTC. Here are another variations:

- AOTC has a four-year restrict per scholar. The LLC has no cut-off dates.

- AOTC requires at the very least half-time enrollment whereas the LLC may be for a single course.

- AOTC has a refundable credit score whereas LLC doesn’t. So, the LLC can solely offset taxes due.

- For tax 12 months 2022 the MAGI phase-out vary for AOTC and LLC are the identical ($90,000 or much less for single and $180,000 or much less for married submitting collectively). To obtain the total credit score (no phase-out), the quantities are $80,000/$160,000.

- The AOTC is per scholar, whereas the LLC is per taxpayer.

While there isn’t any “double dipping” with the 2 credit, you need to use the credit on the identical return so long as they don’t seem to be for a similar bills and the identical scholar. So, it’s possible you’ll use the AOTC for bills for a kid going into her freshman 12 months of faculty when you make the most of the LLC for bills associated to a web based graduate course of your personal, for instance.

Student Loan Interest Deduction

Even nicely after a scholar has walked throughout the commencement stage, scholar mortgage funds generally is a substantial price range line merchandise. If you might be paying curiosity on a scholar mortgage, you might be able to deduct as much as $2,500 of your curiosity expense per 12 months. The phase-out based mostly on MAGI begins at $70,000 and is eradicated at $85,000 for single filers ($145,000 – $175,000 for married submitting collectively filers).

This scholar mortgage curiosity deduction can’t be used for both AOTC or LLC. But identical to you may make the most of each an AOTC and LLC on the identical return, you can even take an curiosity deduction in your scholar loans.

In addition to the tax credit and deductions obtainable, it’s additionally prudent to contemplate maximizing tax advantages by planning for instructional bills early and setting apart funds to speculate with tax-free earnings in certified plans (reminiscent of 529s or Coverdells). Even should you’re planning to assist a grandchild’s training, for instance, the tax financial savings attainable by setting apart funds nicely upfront with certified plans will simply eclipse the tax credit from funding for training bills as they’re incurred.

One of essentially the most rewarding experiences for a mum or dad is sending your youngster off to school after years of preparation. While this may be an thrilling time for fogeys and college students alike, understanding what authorized modifications to count on can assist your loved ones be prepared for sudden circumstances of many sorts. Similarly, tax incentives for such a significant funding in a toddler’s future can reduce the monetary burden. As with many main life occasions, the recommendation of your loved ones’s monetary planner, accountant, and lawyer can information you thru this transition.

Read More From Our Partners at TurboTax:

Editor’s Note: The opinions expressed on this article are these of the authors. The content material was reviewed for tax accuracy by a TurboTax CPA professional.

Source: www.thestreet.com”