Odds are, the final time you went buying on-line, you had the choice to make use of a “buy now, pay later” (BNPL) app at checkout. Affirm, Afterpay, Klarna, Sezzle, and Zip are only a few of the businesses that supply customers a solution to pay for his or her purchases by way of a collection of mounted installments—with out added curiosity.

According to the Federal Reserve Bank of New York, 20% of Americans surveyed used a BNPL app within the fourth quarter of 2023, and lots of did so to fund their vacation buying. Klarna, Afterpay, and Zip all posted double-digit year-over-year utilization will increase, with $940 million in BNPL purchases going down on Cyber Monday alone.

More and extra customers are turning to BNPL apps as a solution to finance bigger-ticket purchases with out including debt to their bank cards—which, in accordance with Experian, now carry a mean steadiness of $6,501. This is smart given the Fed’s present money-tightening stance, which has brought on the common rate of interest on bank cards (APR) to skyrocket to twenty-eight%, an all-time excessive. Retailers of all stripes are rolling out BNPL cost choices to their prospects, together with massive names like Amazon and Walmart; even bank card corporations at the moment are providing their very own variations of BNPL, and the sky’s the restrict on the varieties of things you can buy, together with all the things from quick meals objects to airline tickets.

So, what’s the catch? There is one. While the convenience and comfort of “buying now, paying later” can’t be beat, should you’re not cautious, missed or late funds may incur charges that add as much as greater than you’d pay should you had used a bank card within the first place. Plus, prospects who default on sure sorts of BNPL funds may finally be penalized with decrease credit score scores, so it’s price understanding simply what you’re stepping into earlier than you click on “accept.”

B4LLS/Getty Images

What is “buy now, pay later?”

The idea of “buy now, pay later” is rather like it sounds: Interest-free loans which might be often payable in 4 installments unfold out each two weeks. These loans are sometimes supplied to web shoppers as a cost choice once they try, however they’re additionally available in shops.

For instance, in case you are making a $100 buy, you could possibly pay for the merchandise (or objects) in 4 installments of $25 with 0% curiosity.

According to the Federal Reserve, there are two sorts of BNPL customers:

- People with low credit score scores (620 or much less) who’ve been denied a credit score software up to now yr. This group makes frequent, small purchases valued at $250 or much less that they may not in any other case be capable of afford.

- Financially steady customers who use BNP on a sporadic foundation on bigger-ticket objects (between $1,750 and $2,000) as a way to keep away from paying curiosity.

Credit issues to each customers, however in numerous methods. The “financially fragile” group chooses to “buy now, pay later” as a result of they’ve little or no credit score, whereas the financially steady group doesn’t wish to incur the curiosity that comes with making a purchase order on a bank card. For each teams, BNPL affords advantages.

Related: What does your credit score rating imply? Ranges, historical past & scoring standards

How does “buy now, pay later” work?

To be eligible for a BNPL mortgage, you could fill out an software, together with your identify, electronic mail tackle, date of start, and telephone quantity. You additionally must have a debit card, bank card, or checking account to make your on-line funds. In addition, you should be not less than 18 years of age.

“Buy now, pay later” corporations make cash from the charges they cost—each to prospects in addition to the companies they companion with. BNPL apps cost companies setup charges and transaction charges. They additionally cost prospects late charges and extra charges for missed funds, which we’ll get to subsequent, since these can play a task in figuring out your credit score rating.

How do BNPL apps have an effect on your credit score rating?

Some individuals suppose that simply because BNPL apps don’t ask you to offer your Social Security quantity, your info received’t be shared with a credit score company—however that isn’t true.

BNPL corporations typically run a credit score examine on their prospects, and relying on which sort they conduct (particularly should you take out a longer-term mortgage), they may report your cost historical past to a credit score bureau, which may influence your credit score rating.

- A tender credit score inquiry features a assessment of your credit score file and different restricted info that doesn’t have an effect on your credit score rating.

- A tough credit score inquiry, or a “hard pull,” is a request in your full credit score report, which stays in your credit score file for 2 years. This has a small (5-point) influence in your credit score rating. However, customers with a number of onerous inquiries over a brief interval are considered by lenders as being credit score dangers, giving the impression that they’re determined for loans that they might not pay again.

In 2022, Forbes reported that the nation’s three main credit score reporting companies, TransUnion, Equifax, and Experian, had integrated BNPL knowledge into shopper credit score information, however this info had but to be included in credit score scoring fashions—however that’s most definitely a matter of when, not if. Each tagged BNPL knowledge individually from mortgage and bank card lending reviews; Equifax mentioned it has been conducting assessments that may finally enable lenders to obtain this info as a part of a shopper’s credit score file.

BNPL customers ought to notice when their funds might be due; late charges on missed funds can vary from just a few {dollars} to as much as 25% of the quantity of the mortgage. And should you default on a mortgage and the steadiness is shipped to collections, credit score bureaus might be notified.

Need to return the merchandise you bought? If you used a BNPL app, issues may get difficult. In a complete report detailing the dangers of BNPL, the Consumer Financial Protection Bureau mentioned that 5% of BNPL customers surveyed had problem acquiring a refund for an merchandise they bought or by no means obtained, as a result of they couldn’t cease the funds.

How are you able to safely use a BNPL app?

The attract of utilizing a “buy now, pay later app” is simply how simple it’s to finance no matter you wish to purchase. That makes it significantly simple to overspend, should you’re not cautious. Stripe, the cost terminal firm, reviews that companies who supply BNPL providers get pleasure from an astounding 27% enhance in gross sales quantity.

So that’s why it’s worthwhile to reiterate just a few greatest practices:

- Before you settle for the phrases of your BNPL mortgage, remember to learn the advantageous print. That manner, you’ll know when your funds are due, the value you have to to pay, and what the penalties are.

- Try to repay your BNPL mortgage in full as quickly as you’ll be able to.

- And, as all the time, don’t purchase what you’ll be able to’t afford.

What is the perfect BNPL app?

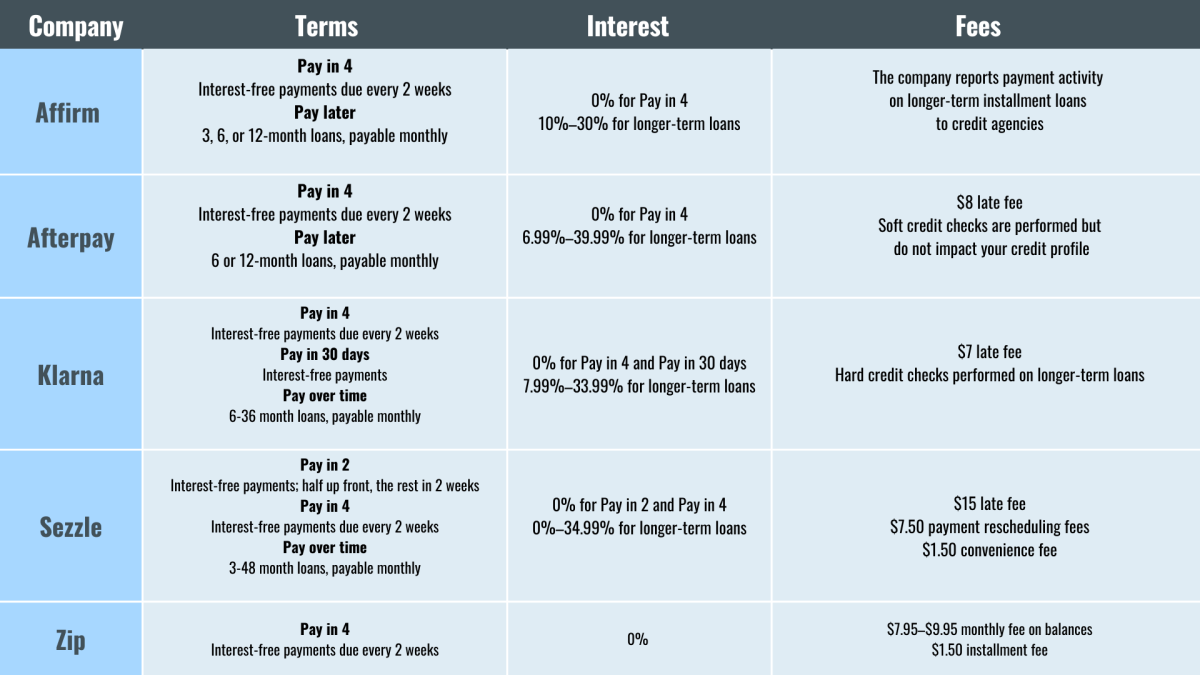

We’ve put collectively a useful chart so you’ll be able to see how the BNPL apps stack up.

“Buy now, pay later” comparability chart

TheRoad

Source: www.thestreet.com”