By Elizabeth Renter | NerdWallet

The Federal Reserve has been on an inflation discount marketing campaign for about 19 months, influencing greater rates of interest throughout the financial system. The rate of interest that could possibly be affecting the best share of households is dear, and one they could have missed.

Ask somebody what their mortgage charge is they usually’ll most likely be capable to inform you. Ask them for the rate of interest on certainly one of their bank cards and put together for a clean stare. But as of the second quarter, we collectively carry greater than $1 trillion in bank card debt throughout some 578 million bank card accounts, in keeping with knowledge from the New York Fed. And the share of American households carrying a bank card steadiness — about 47%, in keeping with an early 2023 NerdWallet evaluation — surpasses that of mortgages (40%) and auto loans (41%).

Average rates of interest charged on bank card accounts have risen from simply over 16% in February 2022, earlier than the Fed started elevating charges, to only over 22% as of May 2023. And in case you carry a steadiness from one month to the subsequent, this quiet enhance could possibly be costing you a whole lot and even hundreds of {dollars}.

Your bank card rate of interest may be simple to overlook

Each month, I log into my bank card accounts, scan the fees rapidly to make sure I’m the one who truly made them, then make a cost. Nine occasions out of 10, I pay the complete steadiness. I don’t spend lots of time on this process, and I don’t search for the rate of interest. I simply don’t. However, within the curiosity of this text, I went wanting.

It took me about 4 minutes to trace it down — not unhealthy, nevertheless it actually wasn’t among the many many numbers on my account’s dwelling web page. Instead, I discovered it by pulling up my month-to-month assertion and scrolling to the final web page. In different phrases, if somebody isn’t actively in search of the rate of interest, they’re unlikely to bump into it and unlikely to know what they’re being charged.

A number of proportion factors can imply a whole lot in curiosity

If you’re not paying off your bank card steadiness every month, you’re possible paying curiosity. I say this matter-of-factly, to not scold. Carrying bank card debt is usually obligatory, and even lengthy after it’s obligatory, it may be a tough behavior to interrupt. That stated, it’s expensive.

There are many strategies for paying off a bank card. Let’s have a look at a couple of choices, and the way a small hike in curiosity adjustments the prices.

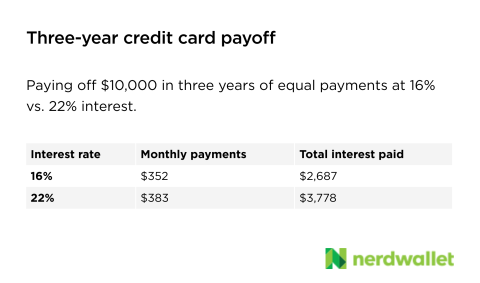

A 3-year payoff plan

Let’s assume you will have $10,000 on a bank card, and have vowed to prioritize paying it off so that you’re not making further purchases. You’ve made a plan to repay the debt in three years and used a mortgage calculator to find out the funds wanted to attain that. If curiosity have been 16%, the month-to-month funds can be about $352 and also you’d pay $2,687 in curiosity over that three-year interval. If you have been as a substitute charged 22% curiosity, the month-to-month funds can be about $30 extra and also you’d pay about $1,000 extra in curiosity over the interval.

Note: For illustrative functions, all cost and curiosity calculations on this article assume the rate of interest is static all through the reimbursement interval.

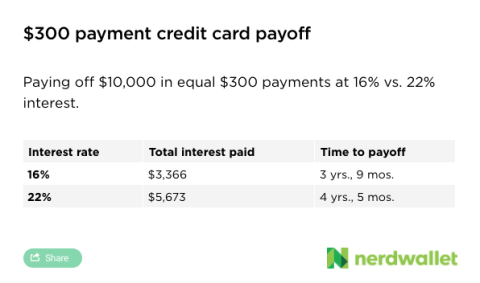

A $300 month-to-month cost plan

Maybe these funds are too steep, however you understand you can also make a constant $300 month-to-month cost.

In that case, paying 16% curiosity on a $10,000 steadiness would take 3 years and 9 months to repay, and price $3,366 in curiosity fees. If you have been paying 22%, it could take 4 years and 5 months, and price about $2,300 extra in curiosity.

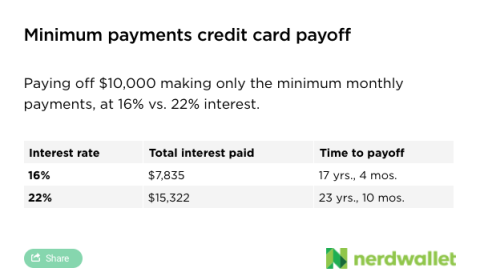

Minimum funds solely

Generally, minimal funds are set at a portion of your steadiness (2%-3%) or a flat charge (sometimes $20-$30), whichever is bigger. And whereas making solely the minimal cost will stop defaulting on the account, it will possibly imply a few years of funds and hundreds of {dollars} in curiosity.

Making minimal funds on a $10,000 steadiness at 16% curiosity would take 17 years and 4 months to repay, and price $7,835 in curiosity. If you have been paying a charge of twenty-two%, it could take 23 years and 10 months, and $15,322 in curiosity.

The backside line

Credit playing cards are a great tool, however curiosity is usually a hefty value to pay for his or her use. Though the distinction between 16% and 22% can simply slip by undetected, it will possibly have a dramatic compounding influence in your potential to get out of bank card debt.

If you’re struggling now to make bank card funds, begin by contacting your card issuer. It would moderately see you pay than not and might be able to work out a decrease rate of interest or completely different due date to assist. If the assistance it supplies isn’t sufficient, take into account credit score counseling by an accredited nonprofit group. A credit score counselor can assist you develop a debt payoff plan and create a funds for longer-term monetary safety.

More From NerdWallet

Elizabeth Renter writes for NerdWallet. Email: [email protected]. Twitter: @elizabethrenter.

Source: www.bostonherald.com”