It was a startling and dramatic second when, in July, the European Central Bank raised rates of interest for the primary time in 11 years.

Not the timing of the price rise – the financial institution’s president, Christine Lagarde, had primed markets for a rise again in June – regardless that it was an occasion on which few would have guess firstly of the yr.

No, it was the extent of the rise, which took the ECB’s primary coverage price from -0.5%, the place it had stood since September 2019, again to zero. It was an even bigger rise than most economists and market contributors had been anticipating.

Markets look much less prone to be caught out once more when, on Thursday, the ECB’s primary policy-making physique, the Governing Council, meets once more.

An increase taking the ECB’s primary coverage price to 0.75%, solely the second time in its historical past that it has raised rates of interest by three-quarters of 1%, is now being priced in by traders. Another half-point rise, as in July, is the very least that’s anticipated.

The purpose for it is because, as within the UK, inflation within the eurozone is rampant.

While modestly decrease than the July headline price of 10.1% within the UK, as measured by the buyer costs index, the estimated headline price within the eurozone of 9.1% for August isn’t far behind.

In a lot of eurozone nations it’s appreciably increased. For instance, Eurostat, the EU’s primary statistical company, estimates that inflation in August was working at 10.5% in Belgium, 13.6% within the Netherlands, 11.1% in Greece and 10.3% in Spain.

In the Baltic trio of Latvia, Estonia and Lithuania, it’s north of 20%. Were it not for the outlier of France – whose anticipated price is simply 6.5% as a result of Emmanuel Macron has capped power costs at huge expense to French taxpayers – the typical headline price of inflation within the eurozone could be nearer nonetheless to that of the UK.

So the ECB has little selection.

President of the European Central Bank Christine Lagarde

Senior officers on the financial institution, such because the German consultant on its govt board Isabel Schnabel, have been speaking more and more stridently about the necessity to come down tougher on inflation.

At the latest get-together of world central bankers at Jackson Hole in Wyoming, Ms Schnabel gave a speech through which she spoke of the “sacrifice” wanted to curb inflation.

As the economics crew at funding financial institution Goldman Sachs informed purchasers on Friday final week: “The inflation picture has deteriorated further since the July meeting…[there has been] a further broadening of underlying price pressures and slightly higher survey inflation expectations. The new staff projections are therefore likely to show a large upgrade to the 2022-23 inflation forecasts.

“Recent ECB commentary has been hawkish, with govt board member Schnabel arguing at Jackson Hole that the ECB must ‘act forcefully’ to ‘carry inflation again to focus on rapidly’. Following her feedback, a lot of nationwide central financial institution governors mentioned {that a} 75 foundation level hike ought to be thought of subsequent week.

“While other Council members – including executive board member [Philip] Lane – have advocated a steady pace of hikes, the pushback against calls to step up tightening has been limited.

“While not a performed deal, we due to this fact assume {that a} 75 foundation level hike subsequent week is extra seemingly than one other half-point step.

“Given market pricing, a 50 basis point hike would be a significant dovish surprise that we believe would be difficult to communicate in light of the strong inflation data.”

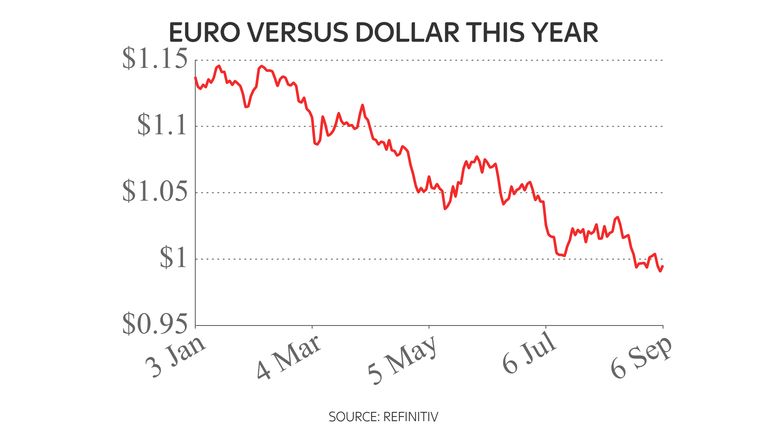

Euro weak point is an inflationary danger for the ECB

An rate of interest rise of this magnitude, although, could be something however pain-free for the ECB.

The eurozone economic system, like that of the UK, is teetering on the point of recession due to the surge in wholesale power costs sparked by Russia’s invasion of Ukraine.

While GDP development in Spain and Italy in the course of the second quarter of the yr was higher than anticipated, due to a correct resumption of tourism to these nations for the primary time because the pandemic, GDP development in Germany, the most important and most vital economic system within the eurozone, has been disappointing.

The newest Purchasing Managers Index (PMI) survey information from S&P Global, a key forward-looking indicator, means that Germany’s companies sector suffered a contraction in exercise in August for the second consecutive month with new enterprise inflows falling for the third consecutive month.

Germany’s big manufacturing sector has additionally been contracting for the final two months. The newest official information from Berlin, printed on Tuesday, revealed that German industrial orders fell in July for the sixth month working.

And in France, the eurozone’s second-largest economic system, the companies sector has been shedding momentum and is at present near stagnation ranges. The consensus amongst economists is that the eurozone is poised for 3 consecutive quarters of contracting GDP.

So, the ECB’s Governing Council can be conscious of the dangers concerned in tightening financial coverage too rapidly regardless that some indicators have been fairly encouraging of late. For instance, partly reflecting tightness within the labour market being seen in different nations such because the US and the UK, the eurozone unemployment price fell in July to a report low of 6.6%.

The greater query for the markets, then, is the place do rates of interest within the eurozone peak – what is called the ‘terminal price’ within the jargon.

Right now, the betting is at round 1.75%, significantly decrease than the place the Bank of England’s coverage price is predicted to peak.

But make no mistake, the ECB can be agonising simply as a lot because the Bank can be over the dangers of elevating rates of interest in the course of a recession.

It is one thing that has not occurred within the UK because the Seventies – and it is going to be unchartered territory for the eurozone.

Source: information.sky.com”