By Elizabeth Renter | NerdWallet

After greater than three years of an interest-free fee pause on federal scholar loans, thousands and thousands of Americans will quickly be on the hook for month-to-month funds. The results might be felt throughout the economic system.

How resuming funds will have an effect on a single borrower varies broadly, relying on, amongst different issues, whether or not they stopped making funds in any respect, how a lot debt they’ve, the compensation program they’re in, and their present and future anticipated revenue. It additionally is determined by the opposite bills competing for a chunk of their month-to-month price range. Because so many individuals are affected — 43.6 million individuals maintain federal scholar mortgage debt, in line with the Department of Education — the impression to the economic system stands to be broad even when some debtors don’t have a tough time adjusting.

Currently, there may be $1.6 trillion in federal scholar mortgage debt excellent, in line with information from the New York Fed’s first quarter Household Debt and Credit Report. This will come down by at the least an estimated $39 billion (about 2.4%) earlier than compensation begins, as long-time debtholders who’ve been paying for 20 years or extra stand to have their slates cleared in a one-time adjustment just lately introduced by the Biden administration.

The White House can be implementing a compensation plan that would considerably cut back the month-to-month funds due for some debtors, and a 12-month “on ramp,” the place debtholders who enter compensation in coming weeks is not going to face repercussions for paying late. These two efforts alone may soften and gradual the financial results of these reentering compensation.

There’s little doubt that doubtlessly lots of of billions of {dollars} in shopper debt coming due will impression the economic system — it represents debt held by roughly 17% of American adults and is the second-largest supply of family debt, in line with the NY Fed report. But the gravity of this impression is but to be decided and more likely to play out over the following a number of months and years. Here are 4 potential financial outcomes I’ll be waiting for within the coming months:

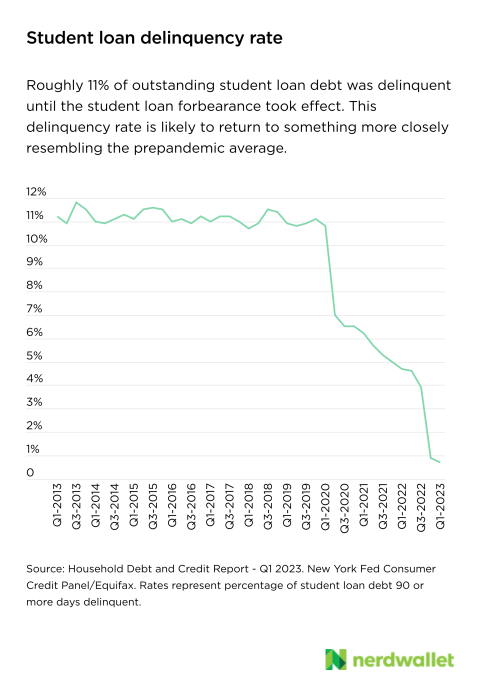

1. Student mortgage delinquencies will rise

In the primary quarter of 2020, practically 11% of scholar mortgage balances have been 90 or extra days overdue, in line with the Household Debt and Credit Report from the New York Fed. The fee pause cleared this slate, and delinquency stands at lower than 1% as of the primary quarter of 2023. That will change. The 12-month on-ramp plan that guarantees to not penalize late funds will delay this impression, however there’s probability that at the least a few of those that struggled earlier than the pandemic will quickly discover themselves again in a well-known state of affairs.

2. Consumer spending will gradual

Pandemic reduction funds and forbearances on mortgages and scholar loans have been only a few of the components that led to households having extra to spend throughout the pandemic. Money that will have in any other case gone to scholar mortgage debt might be used for residence repairs, clothes, or leisure and journey after pandemic restrictions have been lifted. This strong shopper demand has performed a task in higher-than-comfortable inflation charges over the previous few years.

The return of a debt obligation means some households must rein of their spending as soon as once more, and shopper demand will probably fall.

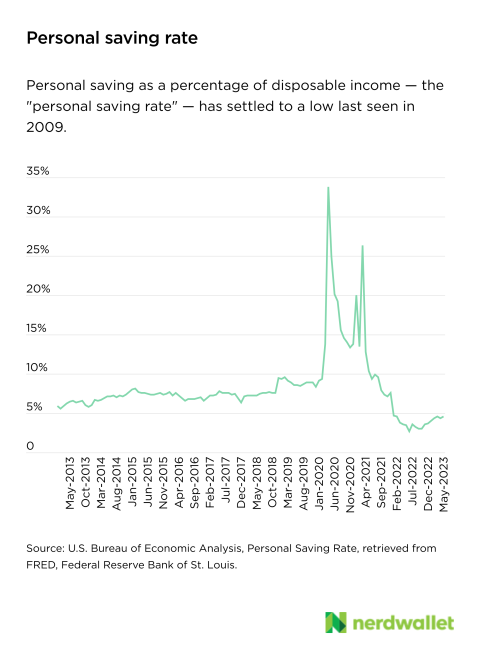

3. Savings will stay low or fall additional

The private saving fee — a share of disposable revenue that persons are capable of put aside after taxes and bills — rose considerably, hitting 34% early within the pandemic, however is now on the lowest because the Great Recession, at 4.6%, in line with the Federal Reserve Bank of St. Louis. With scholar mortgage debt funds coming due, this fee will essentially decline for these affected households.

4. Delinquencies throughout debt varieties could rise

Borrowers on a scholar mortgage fee pause “sharply increased mortgage, auto and credit card borrowing,” a brand new working paper from the National Bureau of Economic Research reveals. Credit card balances initially fell in 2020 as reduction funds got here in and fewer debt funds went out, however that discount in balances was in the end undone. Overall, these balances have been 10% greater by the primary quarter of 2023. And it wasn’t simply on bank cards that balances grew. Total debt balances grew by 19% from 2020 to 2023, in comparison with solely 12% from 2017 to 2020, in line with the Household Debt and Credit survey.

The elevated liquidity, or accessible money, in households with paused scholar mortgage debt could have gone towards residence or auto down funds they beforehand struggled to afford, in line with the NBER paper. Now, having to return to often scheduled scholar mortgage obligations after three years with out funds may depart some new owners (and extra debtholders) strapped. Though the overall share of delinquent debt balances fell from 3.2% to 1.4% within the three-year forbearance interval, representing a distinction of about $215 billion, it’s probably it will in the end settle nearer to the pre-pandemic fee.

How debtors can cope

If you’re nervous about your capability to make full scholar mortgage funds as soon as the forbearance ends, the 12-month on-ramp interval will prevent from default, so take into account easing again into full funds if it’s useful. But bear in mind, your mortgage balances will accrue curiosity throughout this time, so the earlier you may make full funds, the higher. If your funds are just too excessive to handle, contact your mortgage servicer; an income-driven compensation plan could also be match, and a brand new one is ready to launch this fall.

More From NerdWallet

Source: www.bostonherald.com”