By Elizabeth Renter | NerdWallet

American household funds have weathered the fallout of the dot-com bubble, the Great Recession and a pandemic over the past 30 years. Despite these challenges and extra, single-parent households as a complete have truly seen broad monetary enhancements throughout this time.

Some households are higher insulated to emerge unscathed (and even improved) from financial turmoil. On the opposite hand, households with one earner and a number of mouths to feed are at a drawback in contrast with these with a number of incomes when there’s a job loss, excessive inflation, sudden medical bills or hassle in monetary markets, for instance. Measuring the monetary well being of a single-income family in opposition to one with two incomes would uncover few surprises. However, analyzing how the monetary well-being of single-parent households has modified, and the way it’s modified relative to others over time, tells a narrative of sure enhancements and remaining alternatives for progress.

I’m the product of a single-parent family. From the time I used to be 3 years outdated within the early Eighties, my mother raised my older brothers and me solo. Later, as an grownup, I used to be the pinnacle of a single-parent family, elevating my daughter who was born in 2000. Much has modified throughout that point, each in how I skilled the world by means of funds personally and throughout the broader economic system. Charting the family funds of single-parent households throughout a long time underscores these adjustments. Income, internet value and homeownership charges amongst single-parent households have improved dramatically, however these households nonetheless lack insulation from monetary shocks, in keeping with information from the Federal Reserve.

Family funds by means of the a long time

The Federal Reserve’s Survey of Consumer Finances is launched each three years and is a trove of family monetary information. I examined 30 years of the information, from 1992 to the just lately launched 2022 report, to see how my lived experiences aligned with the nationwide image and the way the monetary circumstances of households like mine have modified.

Roughly 30 years in the past, in 1992, I used to be 14 years outdated, residing with my mom and one older brother, whereas my eldest brother was in faculty. During childhood, my mother acquired youngster assist, however we nonetheless certified for the free lunch program in school, a typical proxy for family poverty. She had the great fortune of all the time having a gradual job and put herself by means of faculty whereas elevating us.

My expertise as a mum or dad — starting in 2000 — was completely different in that I didn’t obtain assist funds from one other mum or dad however did qualify for broader public help. When my daughter was an toddler, I acquired EBT advantages or “food stamps,” public housing and Aid to Dependent Children, generally known as “welfare.” I, too, put myself by means of faculty and held down a job from the time she was born. Despite starting my journey as a single mom at a deficit from the place my mom started hers — fairly a bit youthful and with just one supply of earnings — I used to be capable of climb extra rapidly, maybe as a result of I solely had one extra mouth to feed or as a result of authorities and social helps of the period made it simpler to take action.

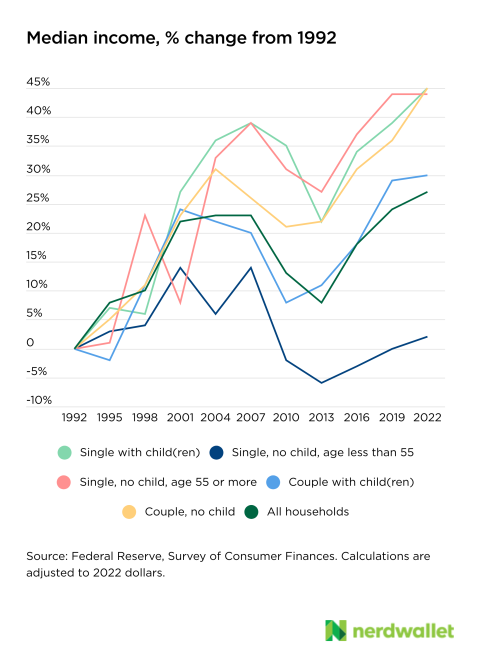

Over the previous 30 years, the median annual earnings of single-parent households has grown simply over 45%, after adjusting for inflation, to $43,000, barely quicker than some other family sort. Across all households, typical incomes grew about 27% throughout that interval.

Note: The Survey of Consumer Finances defines single-parent households as these with kids however not married or residing with a companion.

The next actual earnings means the next lifestyle — your cash can go additional towards paying for the stuff you want. And my private expertise as a toddler and a mum or dad aligns with this information — later in my daughter’s childhood, I used to be higher capable of afford issues my mom would have thought of luxuries once I was younger.

I wish to make it very clear that it’s little greater than a neat coincidence that my private life displays the Federal Reserve information. Much is hidden in nationwide aggregates, and many individuals have their very own anecdotes that may run opposite to the information. In the case of “median income,” for instance, we all know that half of single-parent households earned lower than $43,000 in 2022, and lots of seemingly earned a lot much less. On the opposite hand, half earned greater than that median quantity. And although the nationwide median grew throughout this 30-year interval, some households absolutely skilled durations of declining earnings. Big aggregates enable us to look at broad developments, however in addition they sacrifice some particulars.

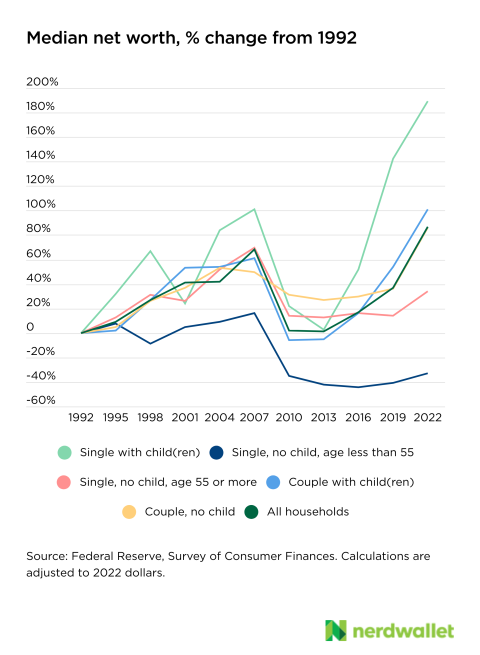

Net value almost triples; houses and retirement belongings climb

Your internet value is the quantity of your belongings (the stuff you personal of worth) minus your liabilities, or money owed. And single-parent households noticed vital will increase in internet value from 1992 to 2022. While households total noticed inflation-adjusted internet value climb 87% throughout this era, these headed by a single mum or dad rose 189%.

The next internet value represents larger insulation from monetary difficulties. When you’ve got extra financial savings, fairness in a house or decrease debt, for instance, you’re higher capable of accommodate sudden bills and higher capable of plan for long-term monetary targets.

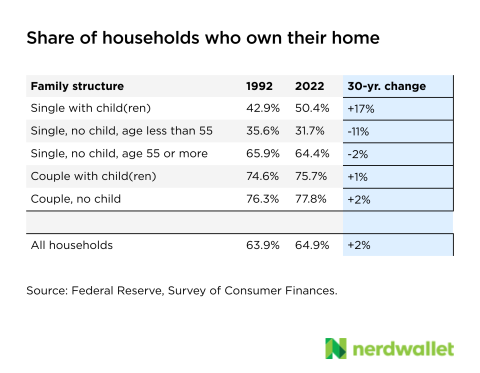

At least a few of this progress in internet value is because of the rise of homeownership amongst single mother and father. The proportion of single-parent households who personal their major residence grew from 43% in 1992 to 50% in 2022, a rise of 17%, and essentially the most dramatic improve amongst all household varieties in the course of the interval.

I used to be raised in leases; my mom hasn’t owned a home since she needed to promote the household residence after my mother and father’ divorce. However, I bought my first residence when my daughter was 7 years outdated, thanks partly to the extra accommodating requirements of an FHA mortgage, down fee help and once I purchased — it was 2007, and residential loans have been being handed out like sweet.

Another necessary asset, retirement accounts, are actually held by 37% of single-parent households, in contrast with 24% in 1992. While a marked enchancment, there’s nonetheless room for progress right here. Among all households, 54% have retirement accounts.

So what can account for these enhancements? It’s seemingly a mixture of things, beginning with a “catch-up” interval. Moms make up 80% of the heads of single-parent households, in keeping with the U.S. Census, and ladies have been afforded the proper to use for credit score and loans similar to mortgages solely in 1974. The full implications of this modification may actually take a long time to work their manner into family private funds and the economic system at giant. Further, the share of single moms who work and the share of ladies going to varsity has elevated over the previous a number of a long time, contributing to elevated incomes energy. And lastly, whereas a 2022 Pew Research Center survey discovered that the stigma of single motherhood is on the rise once more, it’s seemingly nonetheless at a greater place than 30 or 50 years in the past, when authorized protections in opposition to discrimination have been missing.

Where single-parent households can nonetheless acquire floor

The share of single-parent households that get monetary savings truly fell over the 30-year interval examined, from 45% to 41%. In truth, it fell throughout most family varieties throughout this era, although it fell the furthest for single mother and father. Without financial savings, you’re extra more likely to depend upon debt when emergency bills come up and fewer seemingly to have the ability to sustain with month-to-month payments.

Single-parent households are additionally the commonest family sort to revolve bank card debt, or carry it from one month to the subsequent. More than half (52%) of those households carry a stability on their card from month to month, in contrast with 44% of all households, in keeping with the information. Further, single-parent households noticed the best change on this metric amongst all family varieties in the course of the two-year interval capturing the COVID-19 recession — from 2019 to 2022, that share rose 15%.

Carrying bank card debt will increase month-to-month fee obligations, and family payment-to-income ratios mirror this. In any given month, roughly 11% of single-parent households have month-to-month debt funds exceeding 40% of their month-to-month earnings. This 40% threshold is taken into account a measure of monetary vulnerability, and a larger share of single-parent households discover themselves on the incorrect aspect of this line than some other family sort. Further, whereas the share of households over this 40% mark has decreased within the final 30 years, it’s fallen the least in single-parent houses.

Keys to continued enhancements

Overall, typical family funds have improved over the past 30 years, and by some measures they’ve improved most dramatically for single-parent households. But going it alone as a mum or dad, whether or not by selection or by probability, nonetheless presents some larger monetary challenges. Namely, households like mine usually lack the extra security valves afforded households with two potential earners, making them extra susceptible and extra more likely to have to show to debt in durations of monetary stress.

For me, a single mum or dad raised by a single mum or dad, cash choices have been all the time about warning and resourcefulness, being cautious and conscientious about each dime spent and being a scrappy problem-solver when cash was too tight to cowl the entire bills. Honestly, I used to be resentful of this as a toddler. But I used to be grateful for the muse once I grew to become a mum or dad. Early in my daughter’s life, these classes have been essential for retaining the lights on, fairly actually. And now that I’m financially safe, these classes nonetheless underpin how I take into consideration cash and the way I discuss it in my work.

The common funds of single-parent households have improved over time, however particular person family funds can hit setbacks alongside the long-term climb. The path to monetary safety isn’t linear. Incrementally constructing an emergency fund, utilizing debt strategically and understanding the place to show when issues get powerful could make it simpler to rebound and get again on an upward monitor.

The article 30 Years of Change in Single-Parent Household Finances initially appeared on NerdWallet.

Source: www.bostonherald.com”