The Takeaway: You want much less earnings to qualify for a mortgage in some locations within the Midwest and the South than you do within the West. In common, a smaller down fee means the next earnings requirement.

It’s been one other unusual interval for the housing market.

In the primary quarter of 2023, dwelling costs dropped in lots of areas however general mortgage charges ticked up, tightening the monetary squeeze on would-be homebuyers. It’s not excellent news for sellers both. Many are feeling “locked in” to their low mortgage price and have determined to place off itemizing their dwelling till charges come down, including salt to the stock scarcity wound.

DON’T MISS: The 10 Best U.S. Cities For High-Paying Jobs

Housing affordability has improved barely because the finish of final 12 months, in response to knowledge from the National Association of Realtors (NAR). But the standard month-to-month fee of $1,859 on a 30-year, fixed-rate mortgage continues to be a lot greater than a 12 months in the past. In common, households sometimes spend slightly below 25% of their earnings on mortgage funds.

What Should My Income Be Before Buying a House?

Nearly 8 in 10 homebuyers within the U.S. finance their buy. Lenders pay cautious consideration to a possible purchaser’s earnings when evaluating whether or not or to not lengthen a mortgage.

Most lenders want {that a} purchaser spend not more than 28% of their month-to-month gross earnings on their month-to-month housing fee, which incorporates mortgage principal and curiosity funds, plus different recurring prices like householders insurance coverage and mortgage insurance coverage.

Since NAR would not observe knowledge on non-mortgage funds, like insurance coverage, it assumes a decrease debt-to-income ratio of 25% to calculate the minimal earnings a borrower would want to qualify for a mortgage in metropolitan areas.

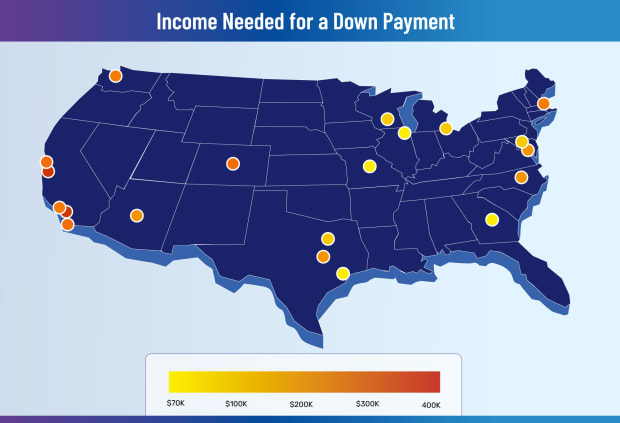

NAR’s newest report for the primary quarter of 2023 revealed {that a} family would want a qualifying earnings of at the very least $100,000 to afford a ten% down fee mortgage in roughly one-third of the 222 U.S. markets it tracks.

National Association of Realtors

For a very long time, the usual down fee for a traditional mortgage was assumed to be 20% of a house’s buy value. A down fee of at the very least that measurement means a purchaser can keep away from the added expense of personal mortgage insurance coverage. Putting down that a lot up entrance also can result in a decrease rate of interest.

But the run-up in dwelling costs has made it more and more troublesome for homebuyers to place 20% down, particularly first-timers. For those that qualify for non-conventional loans from the Federal Housing Administration or VA, there is no requirement—and little incentive—to place down that a lot.

Today, the standard down fee amongst repeat homebuyers and first-time patrons, respectively, is 17% and 6%, in response to NAR’s annual Home Buyers and Sellers report.

How Much Income You Need to Buy a House, by City and Down Payment

Below, we have highlighted the earnings it takes to purchase a home in among the most fascinating locations to stay.

The checklist is customized from Niche’s Best Places to Live in America rating, which evaluates cities on general “livability” utilizing statistics associated to the standard of native faculties, crime charges, housing developments, and the labor market. We pulled NAR knowledge for every metropolis’s corresponding metro space.

In the desk under, you will see the annual earnings you should finance a sometimes priced dwelling in every place with completely different down funds.

Source: www.thestreet.com”