There’s no time higher than the current to get forward of the 2023 tax deadline. A typical query that taxpayers typically ask: “Is it better to owe taxes, or is it better to get a refund?’. Jeffrey Levine, CPA and tax expert for Buckingham Strategic Wealth says there is another option!

Watch the video above to learn more.

TurboTax Live experts look out for you. Expert help your way: get help as you go, or hand your taxes off. You can talk live to tax experts online for unlimited answers and advice OR, have a dedicated tax expert do your taxes for you, so you can be confident in your tax return. Enjoy up to an additional $20 off when you get started with TurboTax Live.

TheAvenue Recommends: Guide to IRS Tax Penalties: How to Avoid or Reduce Them

Quotes| Is It Better to Overpay or Underpay Your Taxes?

Jeffrey Levine, Chief Planning Officer, Buckingham Strategic Wealth

Jeffrey Levine, Chief Planning Officer, Buckingham Strategic Wealth

Recommended Reading: Ways to Increase Your Tax Refund You Never Considered

Video Transcript| Jeffrey Levine, CPA and Tax Expert, Buckingham Strategic Wealth

Robert Powell: Welcome to TheStreet’s tax tips with Jeffrey Levine from Buckingham Wealth Partners. So a common question we get is, is it better to underpay one’s taxes and owe the government money or to overpay and give the government an interest-free loan?

Jeffrey Levine: Are those my only choices? Is that it? My choice is either to dramatically underpay, so I have a penalty or overpay, so I have a massive refund. How about I just do good tax planning, and I pay about what I’m supposed to? And look, here’s the deal. A lot of people know approximately what their tax bill will be from year to year. They have a W-2 income, where they have a relatively stable business, and they take a standard deduction or they have itemized deductions, but they give about the same to charity each year. Their mortgage deduction isn’t changing dramatically from one year to the next. So for a lot of people, their tax bill, it’s fairly determinable even early in the year, right?

Recommended Read: Here’s What Happens if You Don’t File Taxes

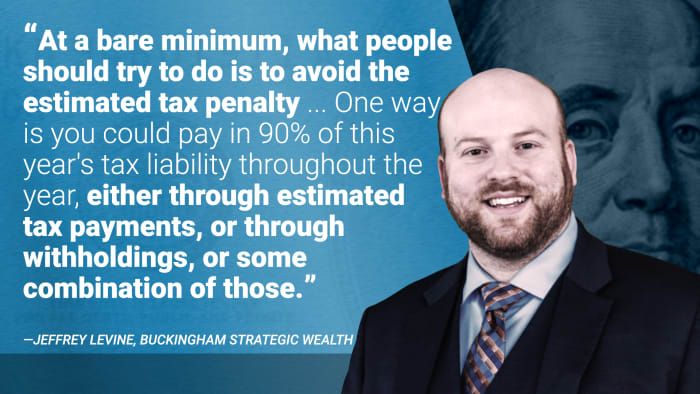

So for instance, right now, we’re early in 2022. You could tell a lot of people about what they will owe in 2022. Now, certainly, for others, that’s not the case. At a bare minimum, what people should try to do is to avoid the estimated tax penalty. In most cases, you want to avoid paying any more than you have to. And so to do that, there are a couple of ways. One way is you could pay 90% of this year’s tax liability throughout the year, either through estimated tax payments or withholdings or some combination of those. The challenge, of course, Bob, is that if you don’t know what this year’s tax bill looks like, how do you know how much to pay? How do you know how much 90% of the unknown amount is?

And so the higher method for lots of people, the protected harbor method, if you’ll, is to base this 12 months’s estimated tax funds on final 12 months’s tax invoice. For most individuals, that simply means paying one hundred pc of final 12 months’s tax invoice all year long. If you’re a excessive earner with greater than $150,000 of revenue, then it is 110 p.c. So for argument’s sake, in the event you had a $20,000 tax invoice final 12 months, most individuals ought to pay $5,000 per quarter this 12 months, and that can eradicate any penalty, even when they owe much more on the finish of the 12 months. So even somebody who wins the lottery, Bob, on May 1st of this 12 months wins $100 million {dollars}. If their tax invoice final 12 months was 20,000, they solely must pay 5,000 every quarter, and they’re going to keep away from the estimated tax penalty. Now come subsequent April, will they owe rather a lot? Yes, however they will not have any estimated tax penalty.

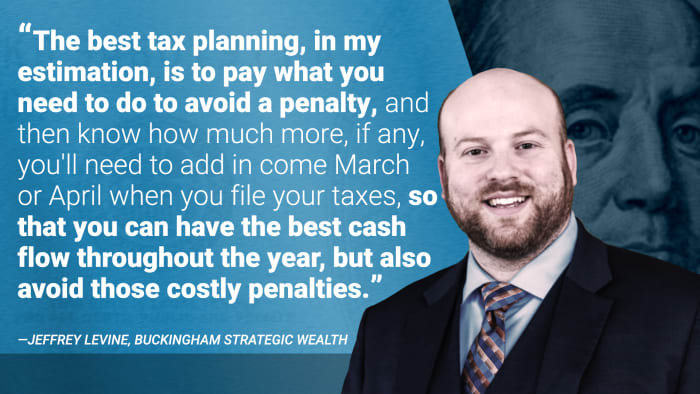

And I’ll end up with one final thought, Bob. It’s that, will they owe rather a lot? Yes, however that simply requires some planning, doing a little proactive work, and never ready till March or April when your tax return is due to have a look at your taxes. But doing it all year long, taking a look at your revenue, taking a look at your deductions, and doing an estimate and saying, are we paying sufficient in? I will surely say that when you have a really massive refund, that is not nice tax planning since you are giving the federal government an interest-free mortgage. And the extra rates of interest rise, which we’re seeing now, the extra pricey that turns into to you. Similarly, you do not wish to underpay to the quantity the place you have got a penalty. So the very best tax planning, in my estimation, is to pay what that you must do to keep away from a penalty, after which know the way rather more if any, you will want so as to add in in March or April while you file your taxes, so as to have the very best money circulate all year long, but additionally keep away from these pricey penalties.

Editor’s Note: Reviewed for tax accuracy by a TurboTax CPA professional.

Source: www.thestreet.com”