Rishi Sunak says we face a “profound economic crisis”. Big phrases, to not point out miserable. But do they actually stack up?

Is the UK actually dealing with one thing distinctive? Can he actually blame a lot of it (as was implicit in his speech) on his predecessor? Or is one thing else happening?

Let’s begin at first.

There is little question that the UK is dealing with robust financial instances proper now. We are fairly plausibly within the enamel of a recession. Look at measures just like the buying supervisor’s index from S&P Global – a measure of how companies are faring proper now – and it’s contraction territory. This is a recession warning, and no mistake.

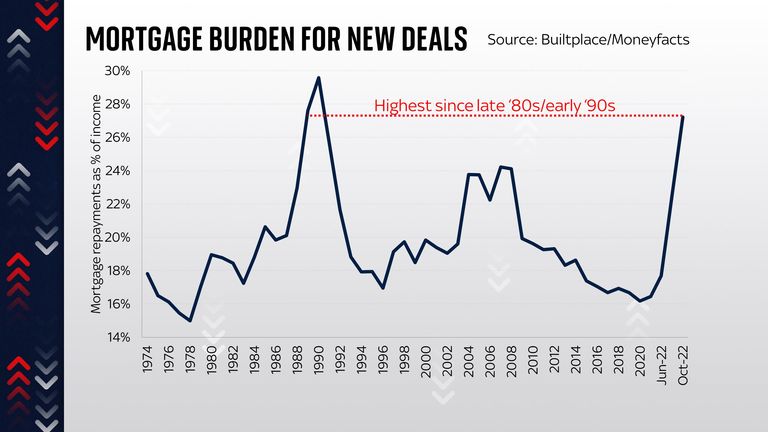

And there are actually some components which is able to make this a grim yr or two for households. For one factor, mortgage prices are rising, and rising quick. The common two-year mounted price mortgage is at the moment up above 6%, a stage which means the best repayments as a share of family incomes for the reason that late Nineteen Eighties or early Nineteen Nineties. This is clearly not excellent news.

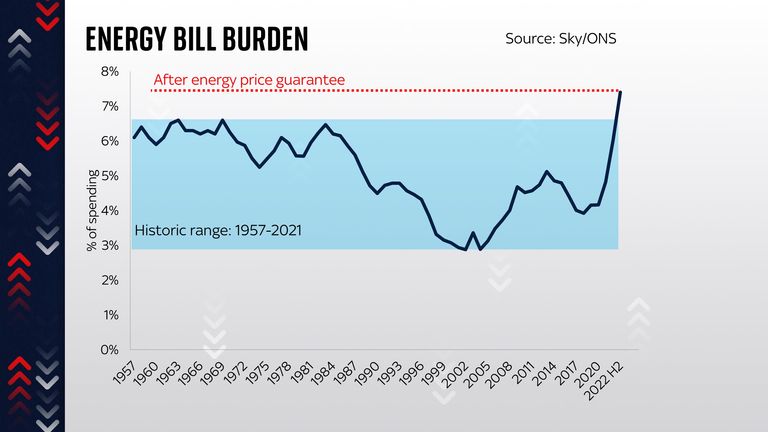

And it is a related story for power payments. Even after you account for the power worth assure launched by Liz Truss, the quantity the typical family spends on power this winter will nonetheless be the best we have seen since a minimum of the Fifties. Again, not excellent news – and be aware that for the reason that scheme has been shortened from two years to 6 months, it is fairly believable the prices are even higher subsequent yr.

Put all of it collectively and any measure of our collective lifestyle suggests an astonishing fall this yr. We are all going to be a lot poorer, relative to what we sometimes need to spend our cash on. And that, largely, is all the way down to the affect of upper power costs, which creep into each a part of our lives.

But these usually are not the one points dealing with the federal government.

The UK just isn’t the one main economic system dealing with a possible recession

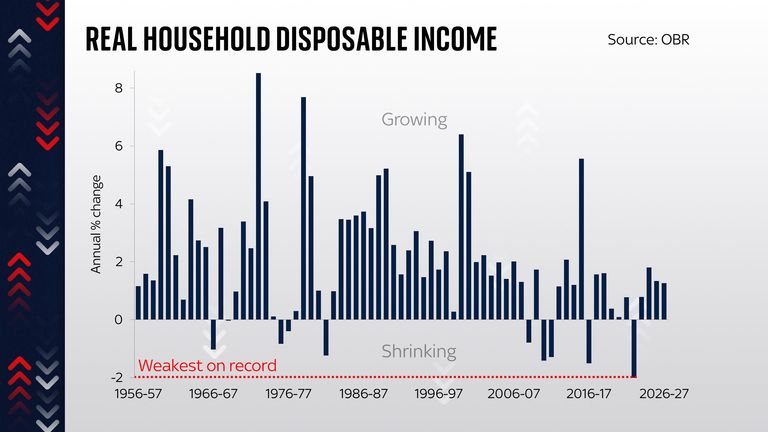

One downside which no earlier prime minister has been in a position to handle efficiently is Britain’s productiveness malaise. Output per hour is maybe the one most vital yardstick of our financial wellbeing and it has basically flatlined for the reason that monetary disaster, making (and this isn’t an exaggeration) every little thing worse: our incomes, our high quality of life, the extent of taxes and nationwide debt.

And that is earlier than you think about the deeper points dealing with the worldwide economic system proper now. Most obviously we appear to be within the early levels of a brand new Cold War, which might consequence within the creation of buying and selling blocs somewhat than a totally globalised world. And this prognosis is, frankly, extra optimistic than many. This can have monumental financial implications.

But here is the factor. None of those challenges are essentially Britain’s alone. The UK just isn’t the one main economic system dealing with a possible recession: others in Europe will most likely have even deeper contractions this winter. Disappointing productiveness is one thing many developed economies wrestle with. Interest charges are rising all over the place (even when the UK’s latest improve in borrowing prices outpaced different nations).

Many of the present issues pre-date Liz Truss

Nor is it particularly honest accountable all these issues on Liz Truss: they beautiful a lot all pre-date her. And here is the actually attention-grabbing factor: the spike in authorities bond yields which adopted her and Kwasi Kwarteng’s mini-budget has now been nearly fully erased.

Those gilt yields are actually almost again to the place they had been earlier than. So too are expectations for Bank of England rates of interest subsequent yr. This is a rare turnaround – a consequence of the truth that the Truss authorities is not any extra.

But it implies that truly a lot of the harm has now been erased. It’s value pondering this for a second. Remember: that rise in gilt yields as worldwide buyers appeared askance on the UK pushed up the potential price of borrowing each for households and for governments. It meant that if the federal government carried on having to subject debt at these sorts of rates of interest then its debt curiosity invoice would have been rather a lot increased. The IFS calculated the continued price at about £10 billion a yr. That’s an enormous deal.

‘Credibility premium’ on authorities debt is shrinking

But now that the “credibility premium” on authorities debt is shrinking, that downside is now not, effectively, an issue. It could quickly have disappeared altogether.

Which raises a query: why did Rishi Sunak attempt to solid such a sombre temper on the steps of Downing Street? My suspicion is that it is about 60% politics and about 40% economics.

The politics first: if he can persuade the general public (and his MPs) that issues are grim, it means much less resistance for the inevitable cuts. Much as Covid united the get together, maybe, he thinks, the specter of financial contagion might do one thing related.

If he can persuade the general public that the unhealthy information he is meting out is all the way down to Liz Truss somewhat than his personal insurance policies as chancellor (most of those issues had been issues when he was in Downing Street and had duty for doing one thing about them) then, effectively, that will clearly go well with him. Even if it isn’t fully correct.

Sunak’s warnings are solely 40% economics

The 40% economics is intriguing, as a result of there is a virtuous circle right here. If he can deploy phrases like “profound economic crisis” and “difficult decisions” he can persuade markets that he is actually critical about slicing debt, which in flip ought to push down gilt yields even decrease. Which means the outlet within the public funds all of the sudden will get smaller too.

Talking robust might truly imply he does not must act fairly so robust within the coming austerity mini-budget or no matter we’ll name it.

Not that a lot of this can be detectable when the fiscal assertion lands. We are clearly in for some robust cuts for the economic system. But many of the challenges they’re supposed to handle had been baked in lengthy earlier than Liz Truss ever reached Downing Street.

Source: information.sky.com”