The tax code bestows largesse upon low-income and high-net-worth taxpayers. This begs the query: which group will get the biggest largesse? Low-income taxpayers can obtain refundable credit, just like the Earned Income Tax Credit, which makes it attainable to get extra money again than is paid in. Wealthy taxpayers enormously profit from the step-up in foundation that wipes out limitless quantities of capital-gain tax. An limitless tax absolution is slightly beneficiant and fairly inconceivable to max out!

So, who will get what? And what does it imply to every of us?

BIO| More About Our CPA and Tax Expert

Bio: Jean-Luc Bourdon, CPA, PFS, Wealth Advisor

Who will get essentially the most invaluable tax breaks?

It’d be enjoyable to survey each teams and ask who they assume Uncle Sam’s favourite nieces and nephews are. But for a extra dependable reply, let’s flip to the Government Accountability Office. The GOA evaluated tax provisions which can be family-oriented, which profit taxpayers beneath sure earnings thresholds, and in contrast them to wealth-oriented provisions.

Recommended Read: What Are Tax Codes

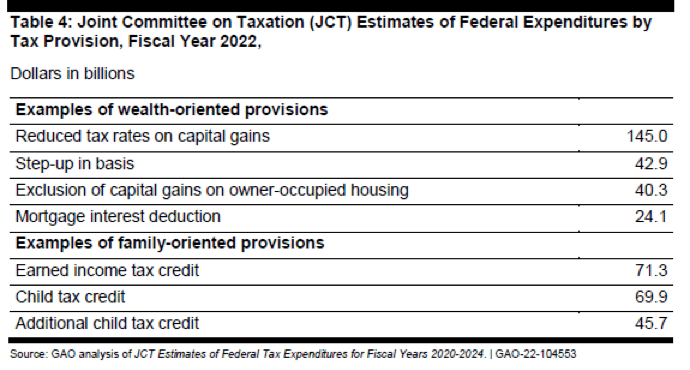

The conclusion: “Tax expenditures for some provisions that are more beneficial to wealthy households (…) are larger than expenditures for family-oriented provisions.” For instance, the desk beneath reveals wealth-oriented provisions whole roughly $252 billion, whereas family-oriented credit whole about $187 billion in income loss.

Source: U.S. Government Accountability Office

The GOA factors out that it hasn’t thought-about each provision within the tax code after all. But I’d say that is ok to offer us a basic concept.

Scroll to Continue

What the tax code means to you

You may conclude that to get the best tax benefits, it’s higher to be rich than a low-income taxpayer. Not so quick. Can’t we be each? Actually, this chance is sort of widespread. Of course, we’ve all heard of billionaires with little taxable earnings. But tax loopholes for tycoons are unique boons. The more and more widespread state of affairs outcomes from a confluence of widespread retirement traits. That means it could possibly be obtainable to the remainder of us.

Reaching tax planning’s Golden Age

Let’s think about three components that have an effect on fashionable retirement. First, as an alternative of getting a pension to pay for retirement, Americans generally accumulate wealth in tax-advantaged accounts, like a 401(ok) or IRA. Second, when relevant, we should begin taking Required Minimum Distributions (RMD) from retirement accounts at age 72. Third, Social Security could make it interesting to delay retirement advantages till age 70. As a consequence, there could possibly be a number of years between the time we retire and the time we should declare social safety and take RMDs. Indeed, in keeping with Gallup, Americans retire of their early 60s.

During this hole interval, retirees might have a excessive web value however handle a low earnings. Think of it as reaching a tax-planning golden age to discover a few of the tax code’s most beneficiant provisions. For instance, some retirees might benefit from the 0% capital-gain tax fee and harvest features to benefit from it. Some who retire earlier than qualifying for Medicare at age 65 may even qualify for a large health-insurance Premium Tax Credit. More usually, it’s an opportune time to contemplate Roth conversions.

Overall, the multitude of choices obtainable for retirement saving, together with taxable, tax-deferred, and tax-free accounts, present varied cash spigots that could possibly be adjusted as wanted to optimize taxation all through retirement. Financial complexity fosters alternative.

Other low-taxable earnings planning alternatives

At the sting of life, excessive medical deductions may trigger low-taxable earnings. Expanded longevity and costly long-term care make this case all too widespread. Then, seeking to totally make the most of medical deductions could be very invaluable. Low earnings may quickly consequence from taking a sabbatical, beginning a enterprise, or caregiving. Any time our earnings falls, the tax code is the juicer for urgent the proverbial lemonade.

To get essentially the most beneficiant tax breaks, it’s clever to construct wealth and optimize intervals of low taxable earnings. Modern retirement typically begins and typically ends with such intervals. Self-funded retirement additionally requires wealth constructing, and the tax code supplies appreciable incentives for it. Wealth-building incentives and low-income tax advantages might mightily merge once we attain planning’s golden age, and the tax code bestows upon us the most effective of each worlds.

More Tax Advice From Our Partners at TurboTax.com:

Editor’s Note: This article is for basic data and academic functions solely and isn’t supposed to function particular monetary, accounting, authorized, or tax recommendation. Individuals ought to communicate with certified professionals based mostly on their particular person circumstances. The evaluation contained on this article could also be based mostly upon third-party data and should turn into outdated or in any other case outdated with out discover.

The content material was reviewed for tax accuracy by a TurboTax CPA knowledgeable.

Source: www.thestreet.com”