Rule 72(t) refers to a piece of the Internal Revenue Code that permits taxpayers to make early withdrawals from sure certified retirement accounts—like a 401(okay) or a person retirement account (IRA)—with out paying additional penalties.

Retirement Daily’s Robert Powell caught up with Jeffrey Levine, CPA and tax professional from Buckingham Strategic Wealth Partners, to debate every thing you want to learn about 72(t).

TurboTax Live consultants look out for you. Expert assist your method: get assist as you go, or hand your taxes off. You can speak stay to tax consultants on-line for limitless solutions and recommendation OR, have a devoted tax knowledgeable do your taxes for you, so that you may be assured in your tax return. Enjoy as much as an extra $20 off whenever you get began with TurboTax Live.

Quotes| Rule 72(t) – Everything You Need to Know

Jeffrey Levine, Chief Planning Officer, Buckingham Strategic Wealth

Jeffrey Levine, Chief Planning Officer, Buckingham Strategic Wealth

Recommended Read: Tax Tips for Retirement

Video Transcript| Jeffrey Levine, CPA and Tax Expert, Buckingham Strategic Wealth

Robert Powell: What is 72(t) and what do you want to learn about it? Well, right here to speak with me about that is Jeffrey Levine from Buckingham Strategic Wealth. Jeffrey, welcome.

Jeffrey Levine: It’s good to be with you, Bob.

Robert Powell: So it’d sound like mumbo jumbo, however 72(t) does imply one thing.

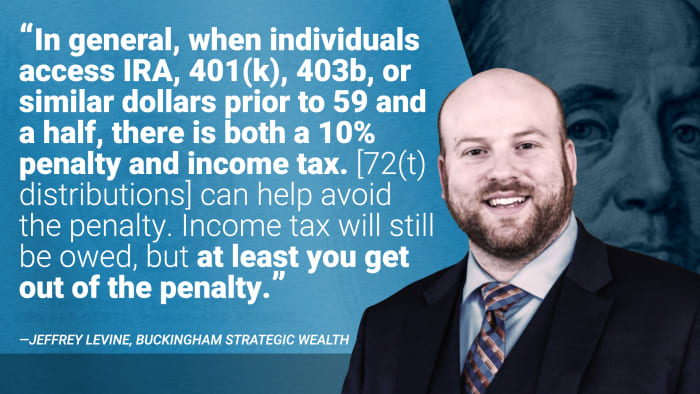

Jeffrey Levine: Well, 72(t) distributions are a solution to get entry to retirement {dollars} previous to 59 and a half with out paying the ten% penalty. In basic, when people entry IRA, 401(okay), 403b, or comparable {dollars} previous to 59 and a half, there may be each a ten% penalty and revenue tax. This will help keep away from the penalty. Income tax will nonetheless be owed, however at the least you get out of the penalty.

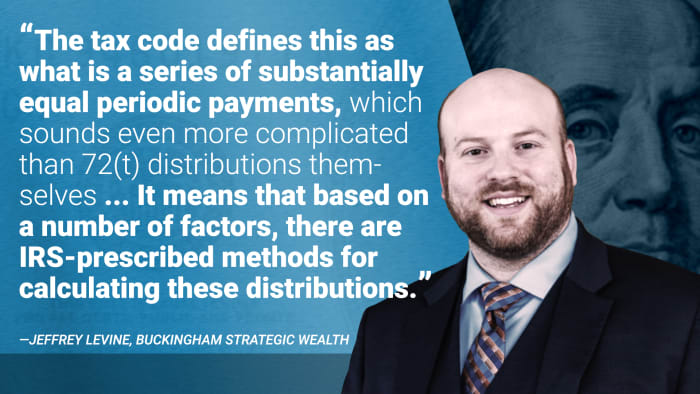

Now, what’s a 72t distribution? Well, briefly, the tax code defines this as what’s a collection of considerably equal periodic funds, which sounds much more difficult than 72(t) distributions themselves. So what does that imply? Well, it signifies that based mostly on plenty of components, there are IRS-prescribed strategies for calculating these distributions. We put in your account stability. We enter sure different issues, corresponding to an IRS-approved rate of interest, and your life expectancy based mostly on plenty of tables. And we provide you with a cost that successfully pseudo annuitizes your account over your lifetime. So you do not actually annuitize it. It’s virtually like a make-believe annuity that you just take out of your account. And by doing so, and by following very, very inflexible and particular guidelines, you are capable of keep away from the ten% penalty on these distributions.

But the 72(t) funds should final for the longer of 5 years, or till you attain 59 and a half, once more, whichever of these is longer. And if you happen to make any errors within the interim, effectively, not solely may it trigger penalties for the distribution that was taken in error, however it’s going to set off retroactive penalties and curiosity on all these 72(t) distributions that had been taken so far.

Editor’s Note: The content material was reviewed for tax accuracy by a TurboTax CPA knowledgeable.

Zach Faulds contributed to the writing of this text and produced the video and/or the graphics related to it.

Source: www.thestreet.com”